Market Insights Overview: Descartes Labs' advanced geospatial insights uses quantitative models for the most accurate price forecasting, and involves a rigorous process from a broad library of forecasts in agriculture/industrial production, weather and human activity. In this blog, we provide you insights on the current week's market.

*Disclaimer: This blog post and related information is provided by Descartes Labs, Inc. (“Descartes Labs”) and was prepared solely for informational purposes. It is based upon or derived from information generally believed to be reliable, but no representation is made that it is accurate or complete. Descartes Labs accepts no liability with regard to the use of or reliance on it, and it should not be taken as investment, trading, or other advice.

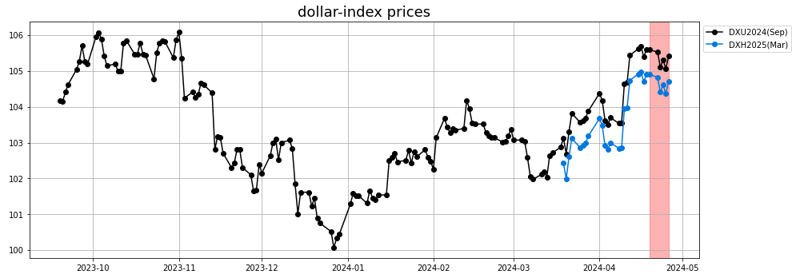

Macro

-

The last couple of weeks have seen the dollar being more stable after the rally we saw earlier in April. Last week macroeconomic news was a bit mixed. We saw some weakening of the dollar after US Q1 GDP was revised downward to 1.6% (q/q annualized) from 3.4%, weaker than expectations of 2.5%, as Q1 personal consumption was revised lower to 2.5% from 3.3%, weaker than expectations of 3.0%, reducing concerns over the risks of an overheating economy. On the other hand, the Q1 core PCE price index was revised upward to +3.7% from +2.0%, stronger than expectations of +3.4%, maintaining a string of data supporting elevated rates.

-

We also saw a weakening of equities earlier in the week.

Grains

There was no major statistics publication for grains and oilseeds over the period.

- Corn: Corn futures are some modest gains over the week across the front months, pulled up by spillover support from wheat and positive Export Sales data.

USDA reported corn bookings of 1.3 MMT for the week of 4/18 in this mornings’ Export Sales report.

While corn dipped over the week before as anticipated by the Descartes Labs forecast, the small rebound from last week was not anticipated. The most recent outlook is flat before a small trough.

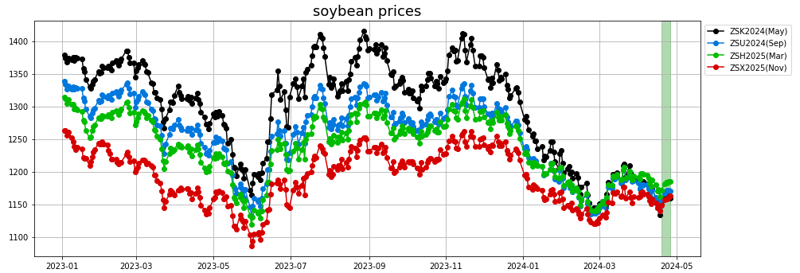

- Soybean: Similarly for soybeans, absent major data, a lot of attention was given to the export numbers published on Thursday. Export Sales data showed just 210,899 MT of soybeans booked in the week that ended on April 18, a 3-week low and below the trade estimates. China was the top buyer of 167,500 MT, as unknown had 136,800 MT in net reductions as they were switched to a destination. New crop sales were on the low side of the trade range at 120,060 MT, less than half of the previous week’s total.

Soybean conditions in Argentina were steady this week at 30% good according to the Buenos Aires Grain Exchange, as poor ratings were up 1% this week to 24%. The crop is 25% harvested, vs. the 48% average pace.

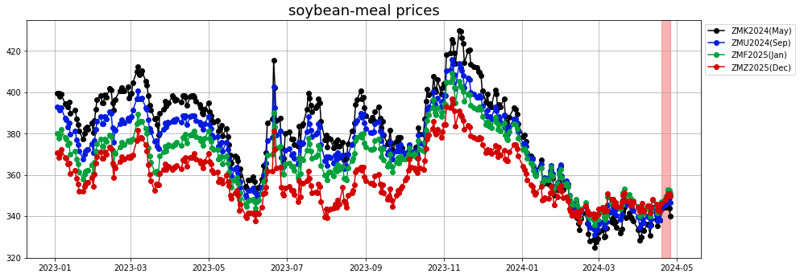

- Soybean meal: Soybean meal sales picked up in the week of 4/18 to 307,859 MT for 23/24, an 8-week high and more than double the previous week.

After anticipating the rally from the lows, the forecast last week was more bearish. The current outlook is for a tight range around 350 before a rally over the first half of May.

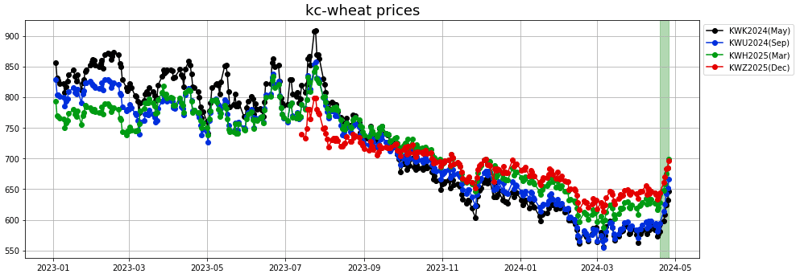

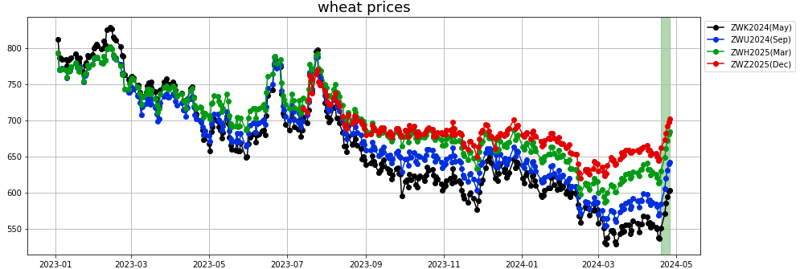

- Wheat: As can be seen in the charts below, wheat was quite supported over last week.

Justifications for the move related to the worsening dry conditions in most wheat growing regions, both in the US and abroad. Portions of the HRW wheat country from western Kansas down to the Texas panhandle are expected to miss out on the widespread rain event over the next week in the central US, with minimal amounts expected. Thursday’s Drought Monitor showed 17.01% of Kansas is now in D2 (severe) drought, up 10.03% from the previous week. Of the whole state, 97.87% is covered in some sort of abnormal dryness.

The 6-10 day forecast also calls for above normal temperatures as we get into May. Eastern Ukraine and parts of Russia are also seeing net declines in soil moisture over the next week, on top of already dry conditions.

Crop conditions in France were also getting worse, with FranceAgriMer pegging the durum wheat crop at 67% gd/ex, down 3%, and the soft wheat crop at 63% a 1% drop on the week.

Vegoils

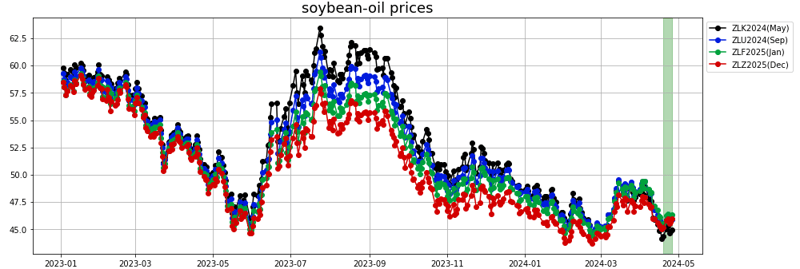

- Soybean oil: The week before last, the vegetable oils market had been under pressure through the sudden weakness in the broader energy complex. On the regulatory front,

on Wednesday, Nebraska’s governor Pillen signed a bill that includes a tax credit for production of SAF. The tax credit is 75 cents/gallon for SAF that meets a 50% reduction in greenhouse gasses compared to fossil based aviation fuel. Such benefit is improving the prospect for long-term soybean-oil demand.

Forecast had been bullish last week in line with the observed price move. The current forecast expects a small consolidation before a small rebound back towards 47 cts/lb.

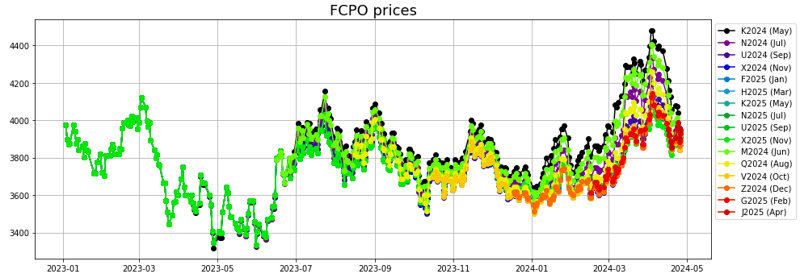

- Palm oil: Palm oil prices trade within a range last week after the large correction observed mid-April. The SBO-CPO differential rebounded after breaching down below 7.5 cts/lb.

Last week forecast anticipated a rebound which did not occur as Palm oil price tread water just below 4000 myr/mt for the July-24 contract. Current outlook is for a small rebound before falling back towards 3700 myr/mt in the first half of May.

Softs

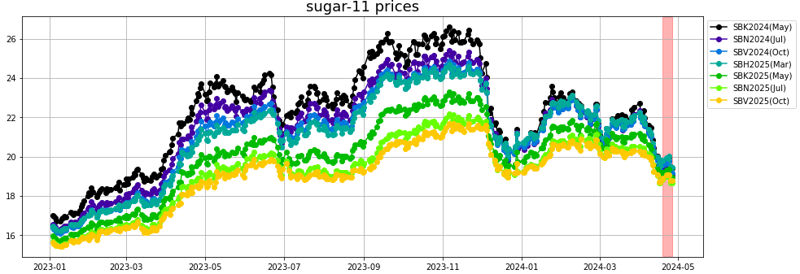

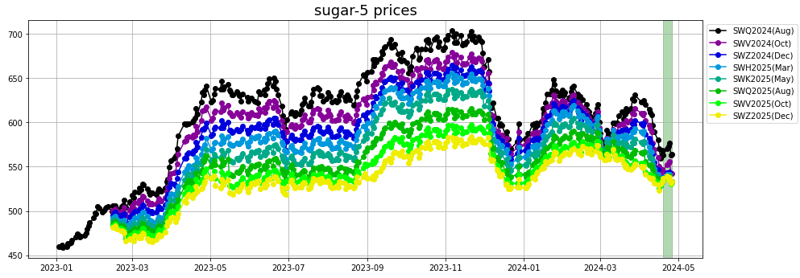

- Sugar: Sugar prices fell back from their best levels today after Unica reported that 2024/25 Brazil sugar production in the first half of April jumped +31.0% y/y to 710 MT. Also, the percentage of sugarcane crushed for sugar production increased to 43.64% from 38.01% last year, signaling increased sugar supplies.

On the bearish side, Conab, Brazil's crop agency, projected Thursday that Brazil's 2024/25 sugar production will climb +1.3% y/y to a record 46.292 MMT as 2024/25 sugar acreage in Brazil increases by +4.1% to 8.7 million hectares (21.5 million acres), the most in seven years. For the 2023/24 marketing year, however, Conab last Thursday cut its Brazil sugar production estimate by -2.6% to 45.7 MMT from a November estimate of 46.9 MMT.

Forecast had been for a stable market last week. The outlook is weaker into early May before a potential rebound towards 20.5 cts/lb by the end of the month.

White sugar: The Indian Sugar and Bioenergy Manufacturers Association reported last Tuesday that India's 2023/24 sugar production from Oct-Apr 15 fell -0.5% y/y to 31.09 MMT as more sugar mills closed for the year and ended their crush of sugarcane. As of Apr 15, 84 Indian sugar mills were still open to produce sugar, compared with 132 mills open at the same time last year.

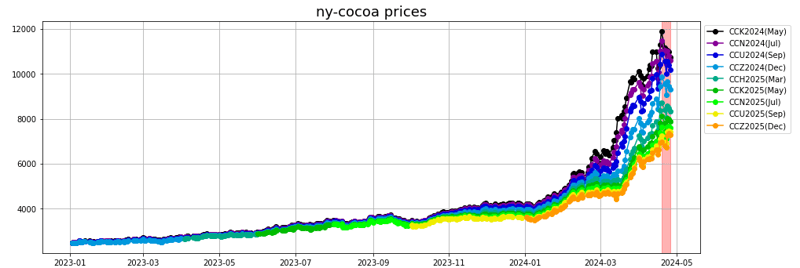

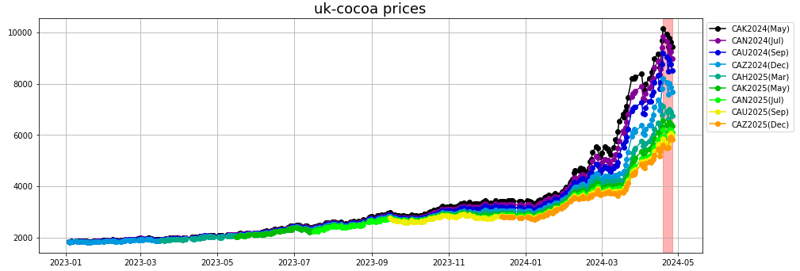

- Cocoa: ICCO projects global cocoa production in 2023/24 will fall by -11% y/y to 4.45 MMT, and global cocoa grindings will drop by nearly -5%, which would push the 2023/24 stock-to-grindings ratio to the lowest in more than 40 years.

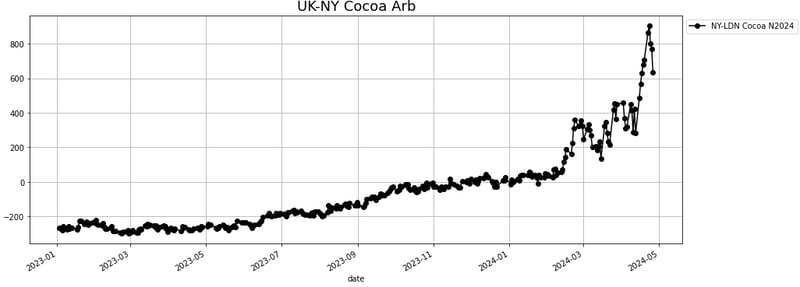

The arbitrage differential between London and New York cocoa reached new levels over the last couple of weeks.

Cocoa prices settled moderately lower on Friday as a stronger dollar fueled long liquidation pressures in cocoa futures. Cocoa also has a negative carryover from Thursday when Nigeria, the world's fifth largest cocoa producer, reported that its March cocoa exports rose +19% y/y to 22,199 MT.

The cocoa market finally corrected down as anticipated by the market, but not after making a new high early in the week. Outlook is for a small rebound from this local low before the sell-off to restart.

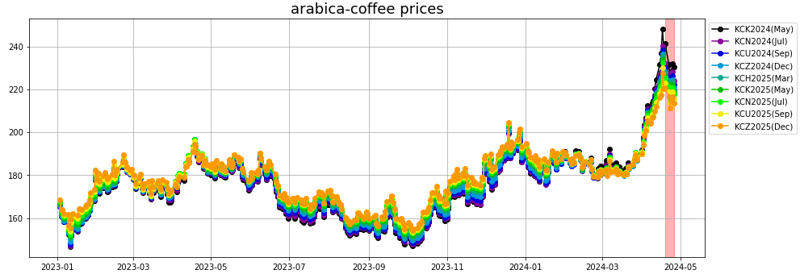

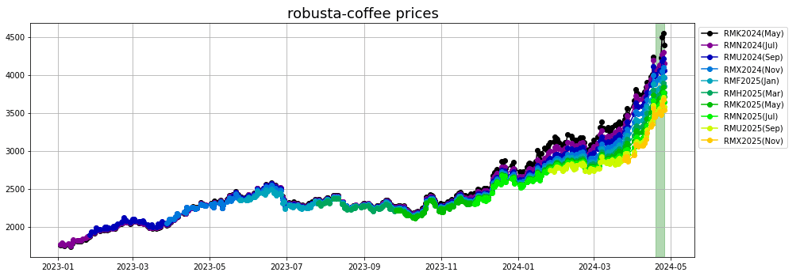

- Coffee: Arabica: Coffee prices on Friday posted moderate losses. A rebound in ICE-monitored coffee supplies sparked long liquidation in coffee futures Friday. ICE-monitored robusta coffee inventories on Thursday rose to a 4-3/4 month high of 3,760 lots, and ICE-monitored arabica coffee inventories on Thursday rose to an 11-1/2 month high of 661,492 bags.

Last Thursday, arabica coffee posted a new 2-year high, and nearest-futures (K24) robusta coffee Thursday posted a new all-time high. Coffee prices have surged over the past two months due to crop concerns in Brazil and Vietnam. Somar Meteorologia reported Monday that Brazil's Minas Gerais region received 7.6 mm of rainfall in the past week, or 58% of the historical average. Minas Gerais accounts for about 30% of Brazil's arabica crop.

Market corrected down last week as expected by the Descartes Labs model. The outlook from here is for a right range around 220 cts/lb.

Robusta: Robusta coffee continues to surge to new record highs on fears that excessive dryness in Vietnam will limit the country's robusta coffee production.

Energy

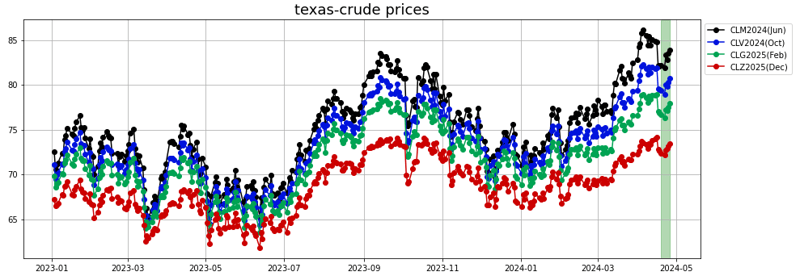

- Crude oil: The US WTI crude oil market did not stay above $85 very long. After an abrupt drop at the end of the previous week, it started to creep back up. On Wednesday, after a series of inventories builds, the US inventories finally drew several million barrels in what may be the start of a tight summer.

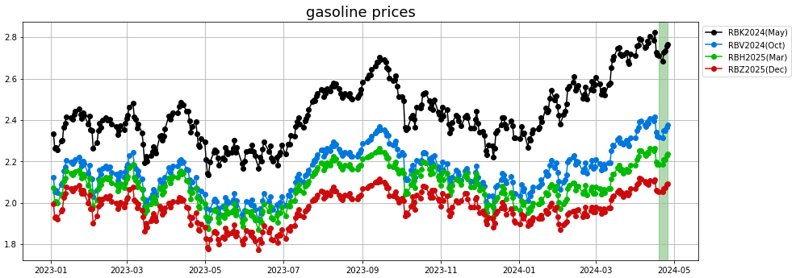

- Gasoline: After an initial correction, cracks for gasoline rebounded over last week. There are still some concerns on demand as the weekly number differential to previous years is widening.

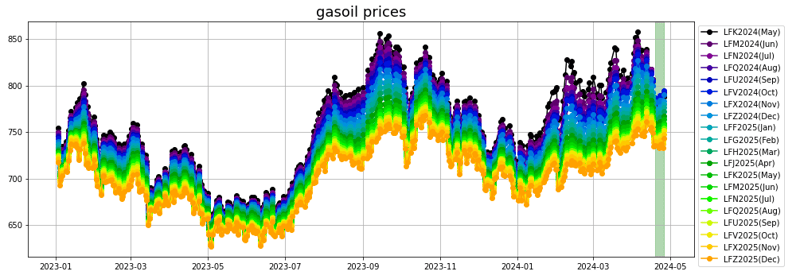

- Diesel/Gasoil: Diesel and gasoil have been the weakest components of the crude complex, with the prompt spreads trading in contango for the last couple of weeks, which had not been seen at any point in 2023.

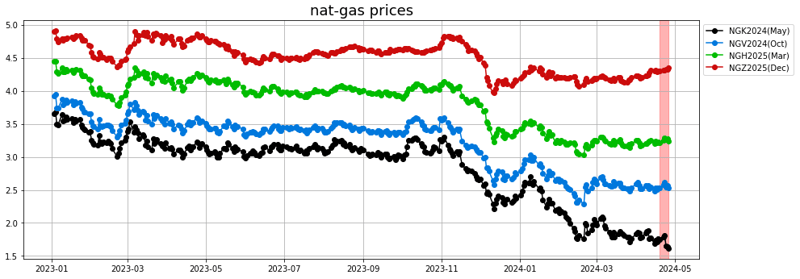

- Natural gas: The situation for the natural gas market on the prompt remained precarious as can be seen from the very large price difference between the prompt month and later in the season. The same topic of low demand in a shoulder period, growing renewable generation eating into the natural gas generation, and LNG export maintenance are making supply plentiful.

Receive Market Report Notifications

Receive Market Report Notifications

Sign up below to get alerts directly in your inbox when a new Market Report is released.