Market Insights Overview: Descartes Labs' advanced geospatial insights uses quantitative models for the most accurate price forecasting, and involves a rigorous process from a broad library of forecasts in agriculture/industrial production, weather and human activity. In this blog, we provide you insights on the current week's market.

*Disclaimer: This blog post and related information is provided by Descartes Labs, Inc. (“Descartes Labs”) and was prepared solely for informational purposes. It is based upon or derived from information generally believed to be reliable, but no representation is made that it is accurate or complete. Descartes Labs accepts no liability with regard to the use of or reliance on it, and it should not be taken as investment, trading, or other advice.

Macro

-

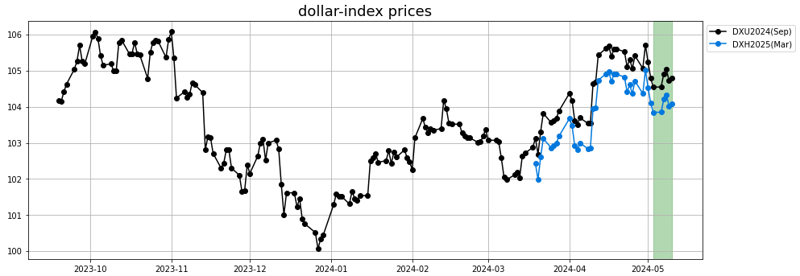

The dollar keeps being volatile compared to a basket of other currencies. Two weeks ago, it weakened quite significantly following some dovish comments from J. Powell from the FED and some confirmation with a Non-Farming Payroll job report on the low side on May 3rd signaling a potentially slowing job markets. This was offset by still solid manufacturing numbers and hawkish comments from other FED governors like Michelle Bowman, which argued it is too soon to consider cutting rates and consider that only one cut in 2024 might be necessary in the end.

-

This hawkishness was offset a bit by a drop in the University of Michigan US consumer sentiment index to 67.4, a 6-month low which pressured the dollar late last week.

Grains

May WASDE report was published on May 10th. In the backdrop, CFTC Commitment of Traders Money Managers net positions showed a significant increase in buying across the grains sector last week and into Tuesday.

- Corn: It was quite a supportive WASDE report for corn, with quite a reduction in ending stocks expectations for the 24/25 crop, both at the US and World level. USDA expects a carry over of 2.1 Bn bu for the 24/25 crop in the US, vs expectations by the market around 2.28 Bn and a number in February WASDE report that was as high as 2.5 Bn.

At the world level, expectations are for 312.3 MMT ending stocks, well below trade expectations around 317.8 and below the carry over from 23/24 crop.

USDA is seeing Chinese imports of corn at 23 MMT, vs 13MMT as expected by China.

The outlook had been more flattish and the model had little anticipation of the rally experienced last week.

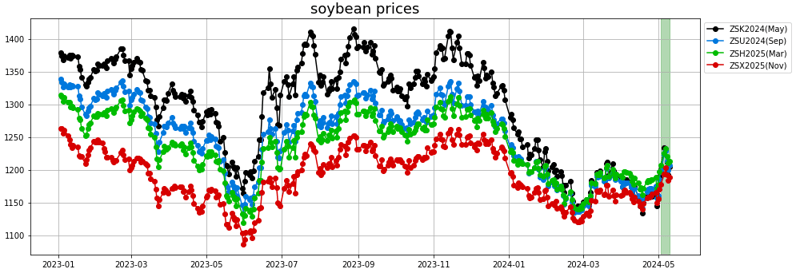

- Soybean: The WASDE update for soybeans was less supportive, even bearish. For the US ending stocks, WASDE reported expectations around 0.445 Bn bu, vs expectations of 0.43 and a number of 0.43 in February report, before the results from the March planting survey. This is the result of a higher production from larger acreage and trend yield, offset by a stronger crush consumption due to higher demand for soybean oil as a biofuel feedstock and higher exports due to the lower and delayed Brazil harvest.

The move up in prices we observed last week was probably more due to a rebalancing in the markets with short positions being closed and new long positions added across the whole sector.

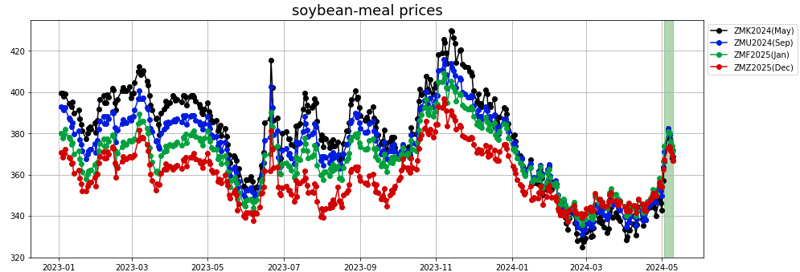

- Soybean meal: Domestic soybean meal disappearance is forecast to increase 3 percent from 2023/24 on increased pork and poultry production. U.S. soybean meal exports are forecast at 17.3 million short tons, indicating a 21 percent share of global trade, compared to the prior 5-year average of 19 percent.

The model had been anticipating some consolidation around 360-370 cts/bu while the meal market continued to improve and breached temporarily the 380 $/ST mark, before coming back down at the end of last week.

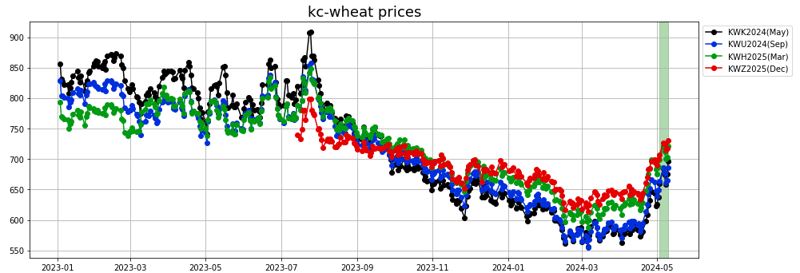

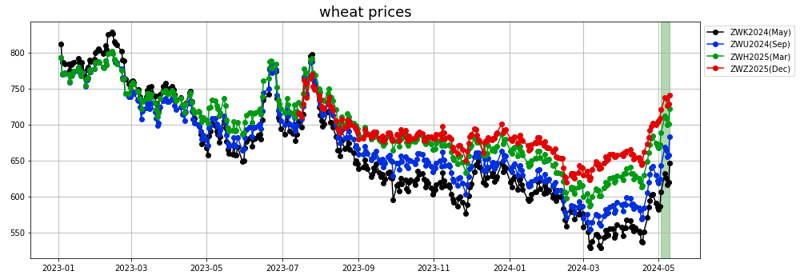

- Wheat: Like corn, US and world ending stocks for wheat pointed to a fairly tight situation. At 0.766 Bn bu of US ending stocks, the WASDE was 0.02 Bn bu tighter than the anticipation by the market. At the world level, the discrepancy was even higher with an estimated 24/25 ending stocks at 253.6 MMT vs expectations by the market at around 257.

While the 24/25 US wheat production at 1.278 Bn bu is higher than the 23/24 production, it is masking different dynamics depending on the wheat type, with Hard Red Winter wheat and White Winter wheat production seen advancing while Soft Red Winter production would be lower YoY by 0.1 Bn Bu at 0.344.

Compared with demand, world wheat supplies among major exporting countries are seen hitting 17-year lows in 2024/25. Stocks-to-use is pegged at 13.5%, near all-time lows.

Vegoils

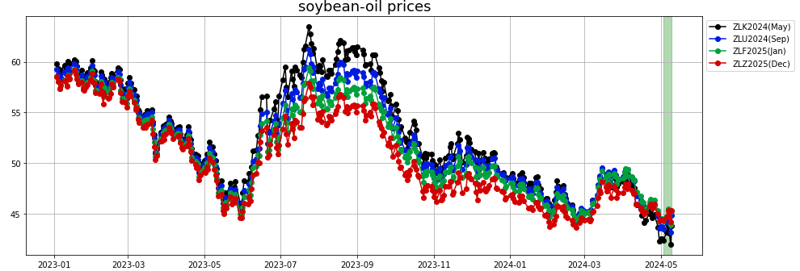

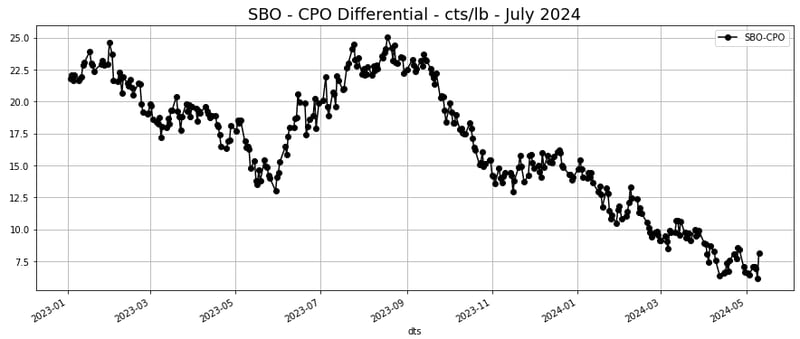

- Soybean oil: Soybean-oil benefited from the support to the soybeans complex and the rest of the grains exports.

Last week's forecast was spot on with a flat outlook for a few days before a small rebound. From those recent levels, the outlook is now flat to up until May 19th, before a small decline expected.

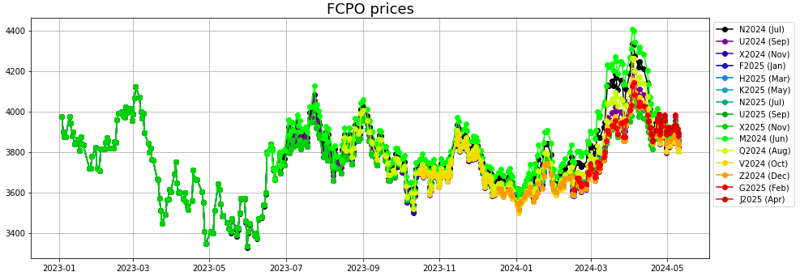

- Palm oil: Palm oil prices trade within a range last week after the large correction observed mid-April.

Last week's forecast anticipated a range bound market which is very much what we observed over the last couple of weeks.

Softs

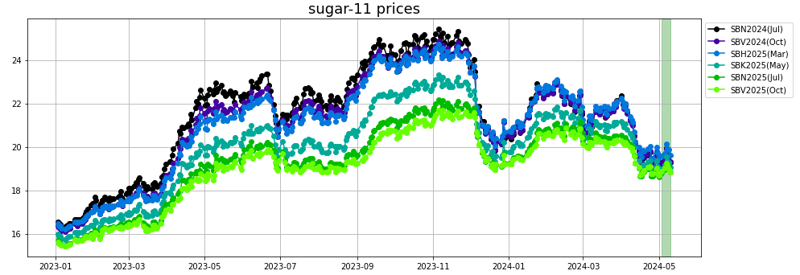

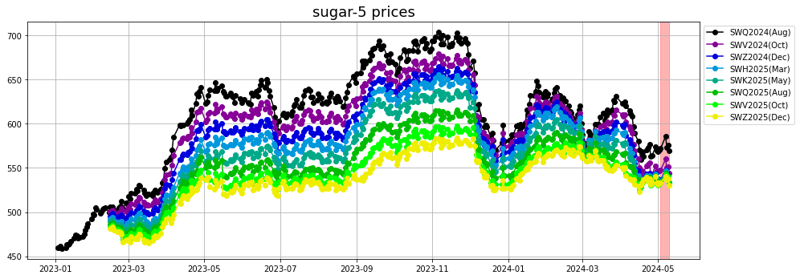

- Sugar: Raw Sugar: During the second half of the week, sugar prices are trading lower on a stronger dollar and on carry-over pressure from Thursday when Datagro raised its 2024 Center-South sugar production estimate to 41.6 MMT from a March estimate of 40.45 MMT.

White sugar: In a bullish update, the Indian Sugar and Bioenergy Manufacturers Association reported Monday that India's 2023/24 sugar production from Oct-Apr fell -1.6% y/y to 31.4 MMT as more sugar mills closed for the year and ended their sugarcane crush. As of April 30, 516 Indian sugar mills had closed operations compared with 460 mills that closed at the same time last year.

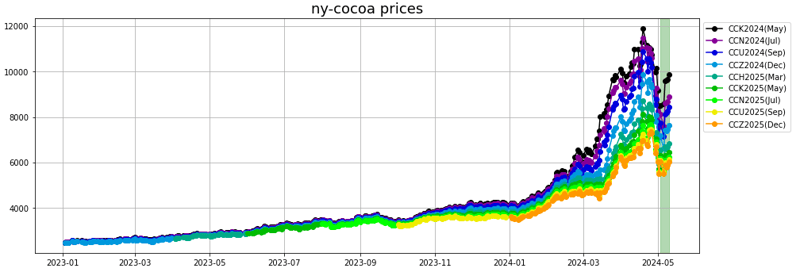

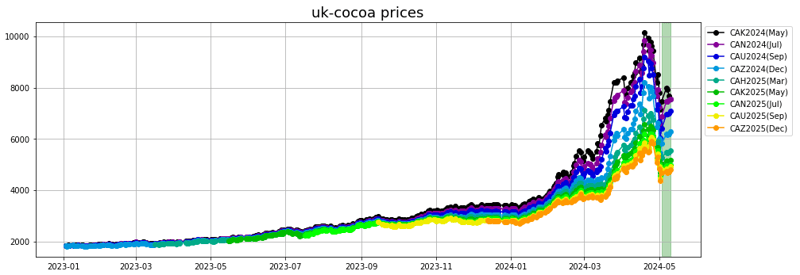

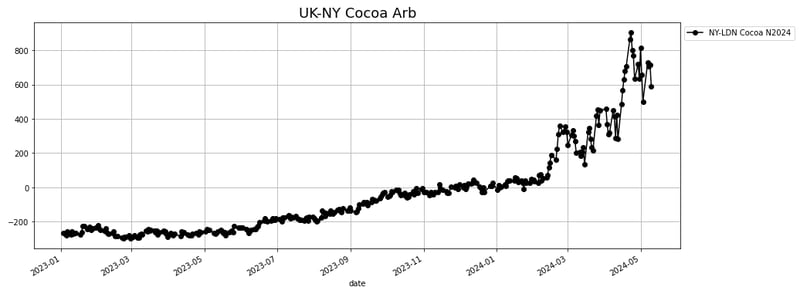

- Cocoa: At the end of last week, Cocoa prices were seeing underlying support today from global cocoa shortages. Cocoa prices plunged from the mid-April record high to a 2-month low in early-May, but have since recovered modestly. Trading conditions remain volatile due to reduced liquidity as high margins caused the liquidation of futures positions. Last Friday's weekly Commitment of Traders (COT) report showed that total long-only positions in cocoa futures sank to the lowest in over three years in the week ending April 23, and short-only positions fell to the lowest in over seven years.

After this move down a couple of weeks that was in line with the forecast at the time, the forecast trajectory had switched to show a rebound that did materialize over the last week. Nevertheless, the forecast trajectory is now showing some consolidation and a drop into the end of May.

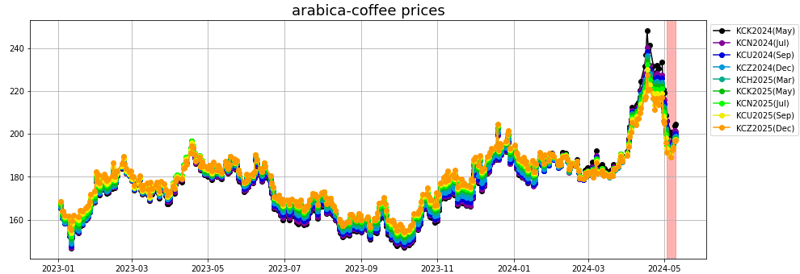

- Coffee: Arabica: Somar Meteorologia reported last week. that Brazil's Minas Gerais region received no rainfall or 0% of the historical average in the past week, the second consecutive week the area has received no rainfall. Minas Gerais accounts for about 30% of Brazil's arabica crop.

The move down, followed by a small rebound, a pattern that we observed last week, was in line with the forecast trajectory. From there, the Descartes Labs model expects some support for the price.

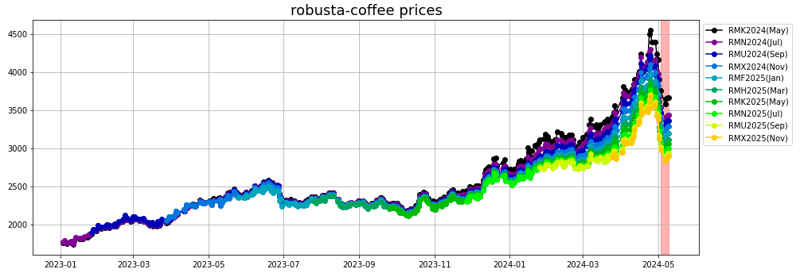

Robusta: Coffee prices have underlying support from insufficient rainfall in Vietnam and Brazil. The Buon Ma Thuot Coffee Association said Thursday that this month's total rainfall in Vietnam's Dak Lak province, a key coffee-growing region, is likely to be 50% lower than last year.

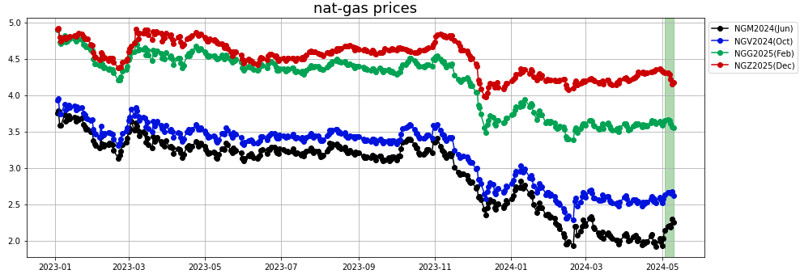

Energy

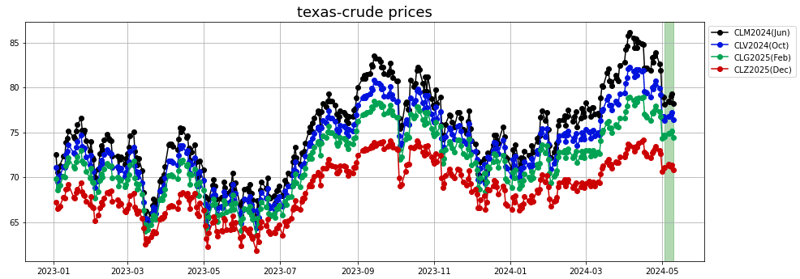

- Crude oil: The crude market was relatively quiet last week. After starting on a weaker footage, the market regains some strength mid week. While the EIA stats release on Wednesday did not show a large draw, the market welcomed the higher refinery runs number which is hinting at the pick up of seasonal number for crude.

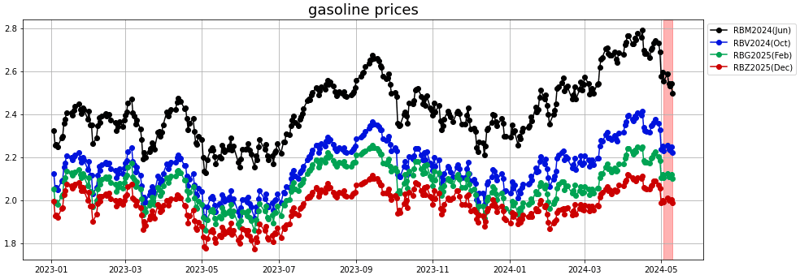

- Gasoline: Gasoline prices weakened vs the rest of the complex last week as the unseasonal inventories build reported, and the associated implied demand, keep showing a fairly large drop in demand YoY.

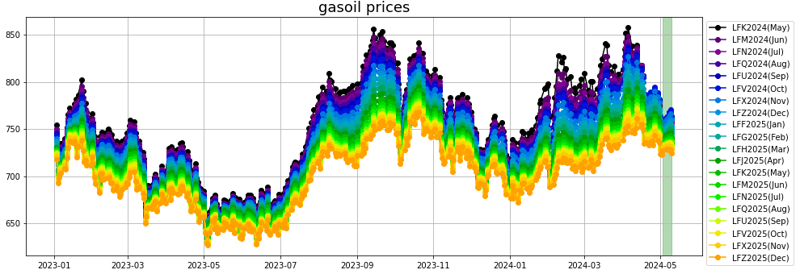

- Diesel/Gasoil: Still no momentum for diesel. The macro outlook appears to slow down, and the large new refineries in the Middle East are expected to ramp up diesel production over the course of the coming months and years.

- Natural gas: It was an interesting situation in natural gas markets last week. Thanks to the strength in the cash market coming from the restart of the Freeport LNG terminal, the very prompt contract of June-24 saw quite a steady rebound the lows, while we saw more pressure further out the curve.

Receive Market Report Notifications

Receive Market Report Notifications

Sign up below to get alerts directly in your inbox when a new Market Report is released.