Market Insights Overview: Descartes Labs' advanced geospatial insights uses quantitative models for the most accurate price forecasting, and involves a rigorous process from a broad library of forecasts in agriculture/industrial production, weather and human activity. In this blog, we provide you insights on the current week's market.

*Disclaimer: This blog post and related information is provided by Descartes Labs, Inc. (“Descartes Labs”) and was prepared solely for informational purposes. It is based upon or derived from information generally believed to be reliable, but no representation is made that it is accurate or complete. Descartes Labs accepts no liability with regard to the use of or reliance on it, and it should not be taken as investment, trading, or other advice.

Macro

-

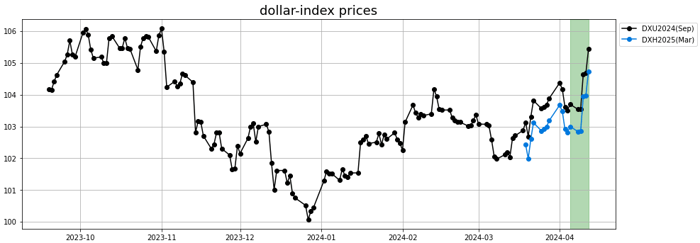

As can be seen below, the dollar-index jumped over the last couple of week to reach a 5 month high.

-

The divergence between the Fed and ECB is boosting the dollar and undercutting the euro, with the Fed expected to delay interest rate cuts and the ECB expected to begin cutting rates in June.

-

Boston Fed President Collins said the strength of the US economy allows time for patience from the Fed, and she is looking into two Fed rate cuts this year.

-

Atlanta Fed President Bostic said he is "not in a hurry" to cut interest rates, and his 2024 outlook is for one rate cut toward the end of the year.

-

The CPI publication on last Wednesday showed an unexpected increase with an annualized number at 3.5% vs the 3.2% expected, justifying more delay in a rate cut by the FED. Probably for a June cut dropped to 25%.

Grains

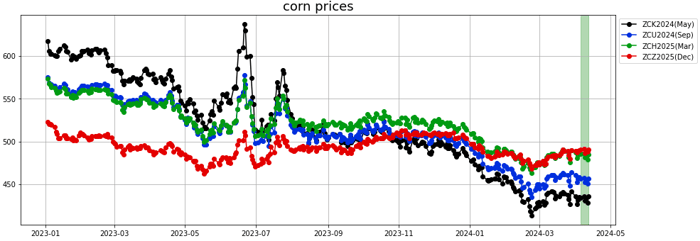

On April 11th, it was the publication of the USDA WASDE Apr-24 report and also publication of updated numbers from CONAB for Brazil.

- Corn: The April report was a bit of a lull especially for US numbers as planting is just beginning. Nevertheless, the Corn ending stocks number was revised lower vs Mar-24 report taking into account the quarterly stocks update.

What is worth noting is that the difference between USDA and CONAB continues, as USDA reported an estimate of corn Brazil production at 124 MMT vs CONAB which revised their number further lower at 111 MMT. Similarly, USDA adjusted their Argentina corn production.

Descartes Labs forecast was a flat outlook over last week. The outlook is for a moderately downward trajectory into the end of April-24 before a rebound.

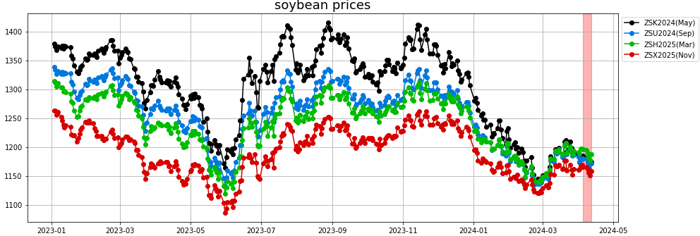

- Soybean: It is a similar story in soybean although the price action was decidedly bearish. The US Ending stocks estimates from WASDE showed an increase to 0.34 Bn bu for soybeans, an increase by 0.025 Bn bu compared to the March report.

Regarding LATAM production, the discrepancy between USDA and CONAB estimates continued with USDA keeping Brazil production at 155 MMT while CONAB adjusted down their numbers again to 146.52 MMT (from 146.9 a month earlier)

On Thursday, the weekly Export Sales report tallied old crop soybean sales at 305,257 MT, a 3-week high and in the middle of the trade estimates.

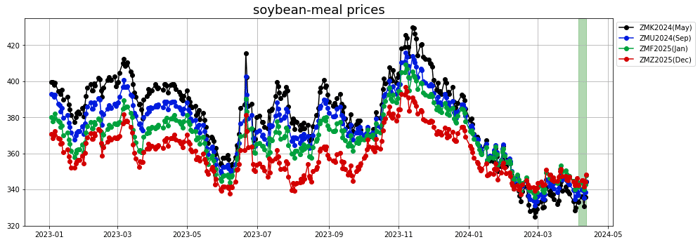

- Soybean meal: There was little news on soybean meal. Price action was on average supportive.

Forecast had been bullish over last week and anticipates a continuation of the upward move.

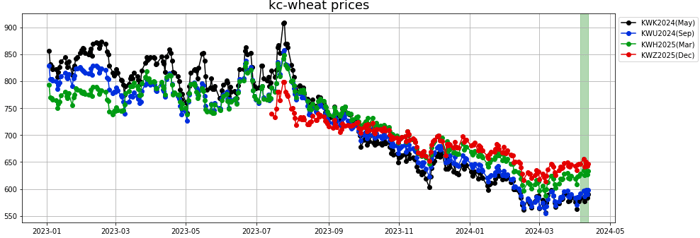

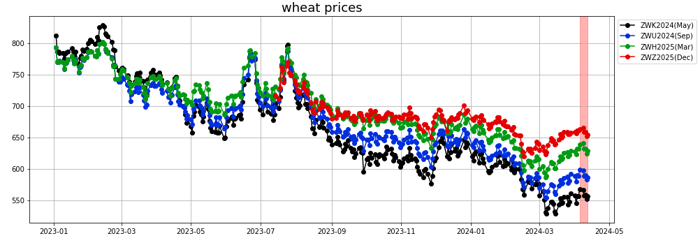

- Wheat: Kansas City Wheat was supported last week while Chicago wheat price contracted a little.

Thursday’s USDA’s WASDE update had a 25 mbu hike to the US carryout number for 23/24 on a 30 mbu drop to the feed & residual use and 5 mbu fewer imports. Stocks were pegged at 698 million bushel and above the average trade estimate (690 mbu).

French soft wheat conditions were rated at 64% gd/ex as of 4/8, a 1% decline from the week prior according to the FanceAgriMer. Last year’s soft wheat ratings were 94% gd/ex, with the current data the lowest for the current week since 2020.

Russia’s ag ministry raised their wheat export tax by 1.3% to 3,276.6 roubles/MT (95 cents/bu) as of April 17 through April 23.

Vegoils

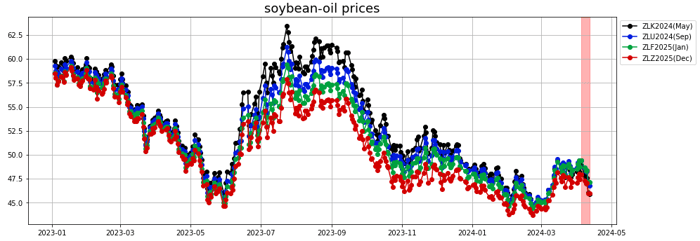

- Soybean oil: Analysts see March 2024 NOPA crush at an all-time record 197.8 mln bu of #soybeans, topping the Dec 2023 high mark of 195.3 mln and up 6% from last March. #Soyoil stocks are expected to have risen 6% during March but stay below year-ago levels. Data is out on Monday but it does appear that such expectations, combined with the bearish soybeans WASDE numbers weighed on soybean-oil prices.

Forecast had been flat to bearish over last week. The drop in prices was sooner than anticipated. As a result the outlook is for a modest rebound before renewed weakness towards 45 cts/lb.

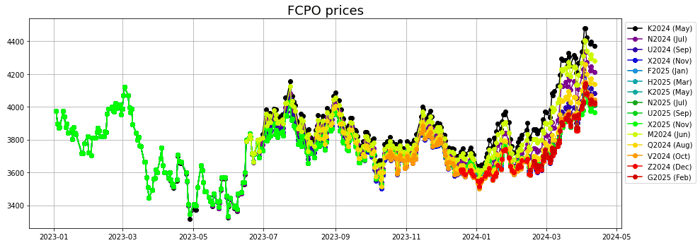

- Palm oil: Forecast had been flat to bearish over last week. The outlook is for a continuation of the correction into the end of April below 4200 myt/mt.

Softs

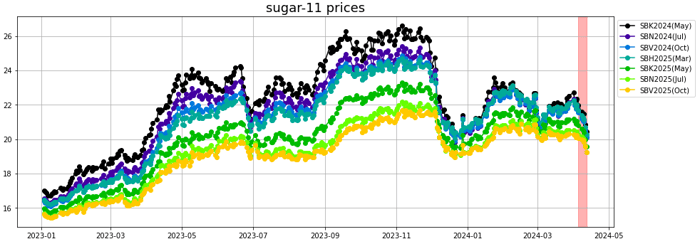

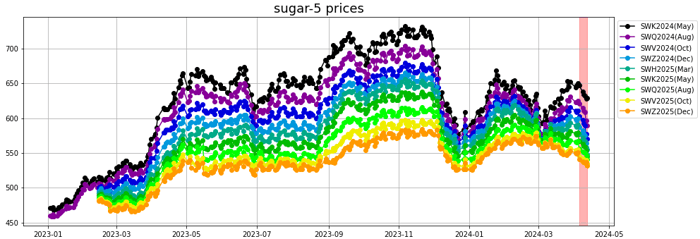

- Sugar: Raw & White sugar: Increased sugar output in Brazil is undercutting sugar prices today after Unica reported Brazil's Center-South sugar output in the second half of March was 183,000 MT, up +9% from last year. Also, Brazilian sugar output so far in the 2023-24 marketing year through March is up +25.7% y/y to 42.425 MMT. Brazil's sugar mills have ramped up their cane crushing for more sugar and less ethanol. Mills have crushed 48.87% of total cane for sugar production this year, up from 45.86% last year.

Weakness in the Brazilian real is also weighing on sugar prices after the real today tumbled to a 6-month low against the dollar. The weaker real encourages export selling by Brazil's sugar producers.

Forecast had been bearish over last week. Descartes Labs model expects a modest rebound followed by further price decline below 20 cts/lb and towards 18 cts/lb.

White sugar: Another bearish factor for sugar was last Wednesday's report from Thailand's Office of the Cane and Sugar Board that showed Thailand's 2023/24 sugar production from Dec-Mar was 8.75 MMT, above a Feb estimate from the Thai Sugar Millers Corp for sugar production of 7.5 MMT.

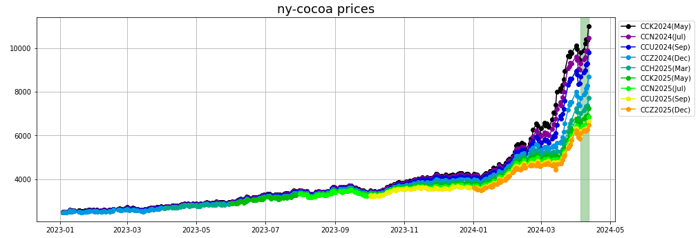

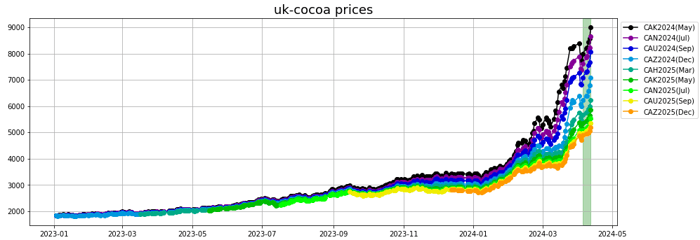

- Cocoa: Cocoa prices today soared to new all-time highs. Concern that global cocoa supplies will continue to shrink in the coming months is pushing prices to new record highs. Due to limited supplies, global cocoa grinders are paying up in the cash market to secure cocoa supplies this year due to growing concerns that West African cocoa suppliers may default on supply contracts.

Bloomberg reported Thursday that the Ghana Cocoa Board is negotiating with major cocoa traders to postpone the delivery of at least 150,000 MT to 250,000 MT of cocoa until next season due to a lack of beans. Cocoa prices have rallied sharply since the beginning of the year, driven by the worst supply shortage in 40 years.

Monday's government data showed that Ivory Coast farmers shipped 1.3 MMT of cocoa to ports from October 1 to April 7, down by 27.8% from the same time last year.

Forecasts had remained bearish as of last week and did not anticipate a continuation of the rally. The outlook is again for some weakness followed by a rebound.

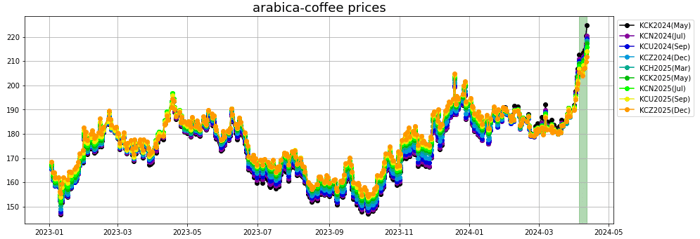

- Coffee: Arabica: Arabica coffee posted a 5-3/4 month high Monday on weather concerns in Brazil as Somar Meteorologia reported Monday that Brazil's Minas Gerais region received 2.5 mm of rainfall in the past week, or 12% of the historical average. Minas Gerais accounts for about 30% of Brazil's arabica crop.

Arabica coffee Wednesday initially moved lower after Cecafe reported that Brazil's Mar green coffee exports jumped +41% y/y to 3.9 million bags. Brazil is the world's largest producer of arabica coffee beans. Weakness in the Brazilian real is also bearish for coffee as the real on Wednesday dropped to a 1-week low against the dollar. A weaker real encourages export selling from Brazil's coffee producers.

Forecast had been bearish for the past week. The outlook trajectory is still bearish for the short-term with a retracement towards 206 cts/lb expected.

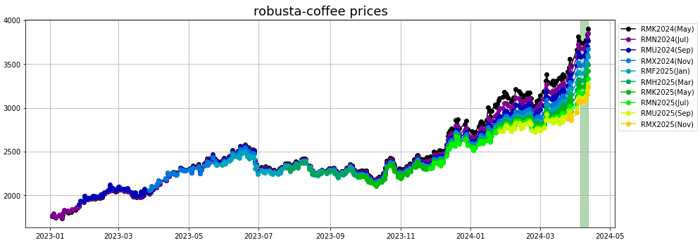

Robusta: Robusta coffee posted a record high last Thursday on fears that excessive dryness in Vietnam will limit the country's robusta coffee production.

Energy

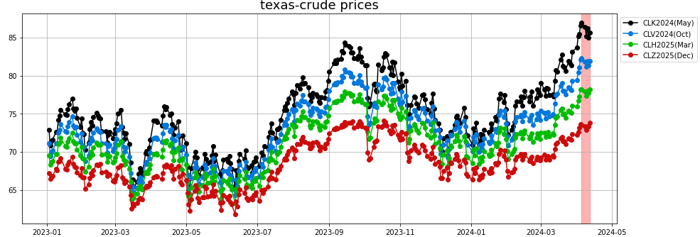

- Crude oil: Despite the prospects of Iran retaliation on Israel, crude markets closed slightly down on the week because of the bearish impact on demand of inflation and more sustained tighter market conditions. With the effective drones launch over the week-end, the crude market is nevertheless likely to open higher on Monday.

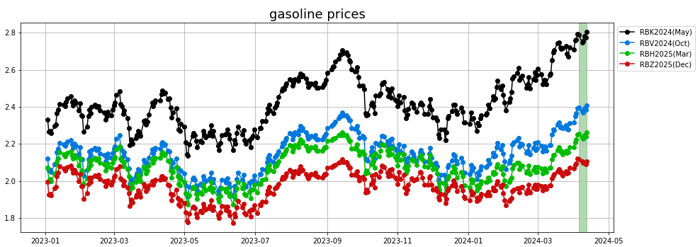

- Gasoline: The attacks on Russian refineries and prospect for lower clean products availability in EU have supported gasoline over the week, despite a slightly bearish stats publication on Wednesday by EIA.

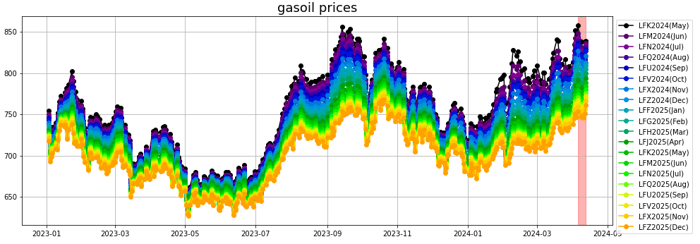

- Diesel/Gasoil: Diesel was negatively impacted by building stocks and contango in the physical market. In addition, the tighter expected monetary decisions would affect demand negatively.

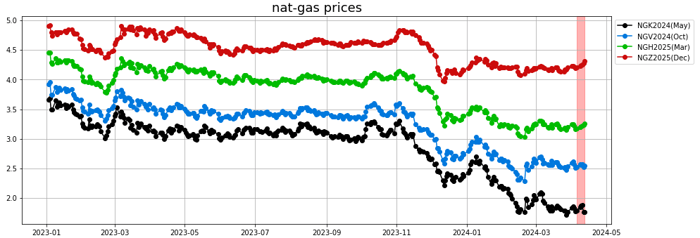

- Natural gas: The natural gas market was relatively unchanged over the last week, especially in the front as support from lower supplies was offset by LNG train maintenance and a bearish demand outlook for the shoulder months of April and May.

Receive Market Report Notifications

Receive Market Report Notifications

Sign up below to get alerts directly in your inbox when a new Market Report is released.