Market Insights Overview: Descartes Labs' advanced geospatial insights uses quantitative models for the most accurate price forecasting, and involves a rigorous process from a broad library of forecasts in agriculture/industrial production, weather and human activity. In this blog, we provide you insights on the current week's market.

*Disclaimer: This blog post and related information is provided by Descartes Labs, Inc. (“Descartes Labs”) and was prepared solely for informational purposes. It is based upon or derived from information generally believed to be reliable, but no representation is made that it is accurate or complete. Descartes Labs accepts no liability with regard to the use of or reliance on it, and it should not be taken as investment, trading, or other advice.

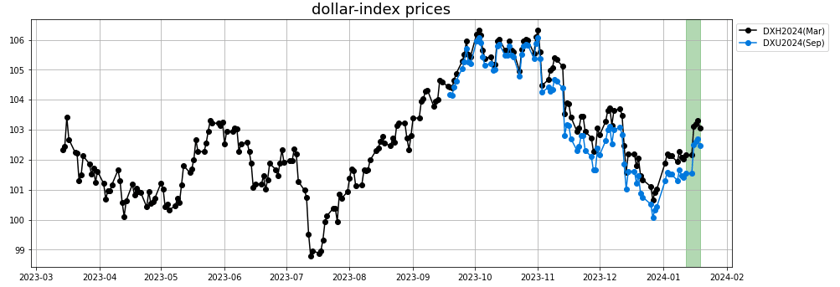

Macro

- The dollar was supported by hawkish comments from the Federal Reserve.

- Comments Friday from San Francisco Fed President Daly were slightly hawkish and positive for the dollar when she said it's "premature" to think that interest rate cuts by the Fed "are around the corner" and that she needs to see more evidence that inflation is on a consistent trajectory back to 2% before easing policy.

- The markets are discounting the chances for a -25 bp rate cut at 3% for the next FOMC meeting on January 30–31 and a 48% chance for that -25 bp rate cut for the following meeting on March 19–20.

- On the negative side, December existing home sales unexpectedly fell -1.0% m/m to a 13-year low of 3.78 million versus expectations of a +0.3% m/m increase to 3.83 million. Conversely, the University of Michigan U.S. January consumer sentiment index rose +9.1 to a 2-1/2 year high of 78.8, stronger than expectations of 70.1.

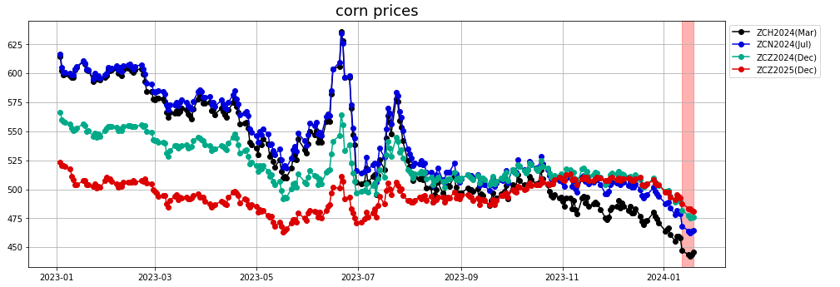

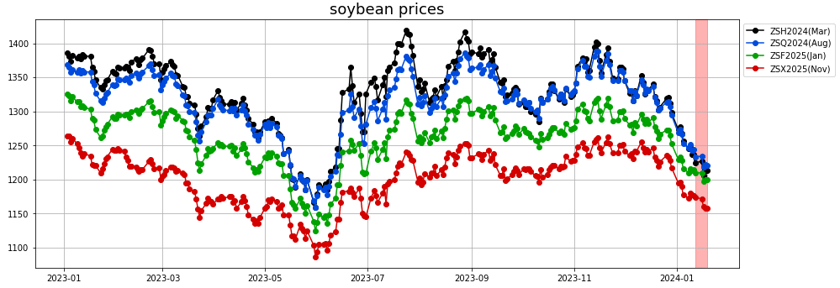

Grains

January WASDE was published ten days ago on Friday, January 12.

- Corn: USDA updated the corn yield expectations to 177.3 bu/acre, much higher than the 175 November number. This was offset to some extent by a decrease of harvesting area to 86.5 (from the 87 millions acre) leading to 15.42 Bn bu.

US Ending stocks were also revised higher to 2.162 bn bu (vs 2.13 vs December 23 and even lower market expectations around 2.1). World ending stocks for corn were also revised higher to 325.22 MMT.

A weekly USDA report showed U.S. corn and wheat export sales for 2023–24 exceeded analysts' estimates in the week ended January 11.

The move down was not anticipated by the Descartes Labs model which had started to be more supportive. Latest forecast trajectory is now quite bullish towards 489 cts/bu.

- Soybean: Soybean remained under heavy pressure over the last couple of weeks. The USDA WASDE update was not very supportive especially for US 2023/24 expected crop with a yield updated to 50.6 bu/acre (from 49.9 in December update). Harvested area was also revised lower but still resulting in a higher production number overall. US ending stocks were raised to 0.28 bn bu, increasing further the stocks to use ratio.

Worldwide, USDA revised down the Brazil production expectations from 161 to 157 MMT, while increasing the one for Argentina from 48 to 50 MMT. A recent analyst from the Rosario exchange in Buenos Aires was quoted as saying that the rain over the last few weeks have been extremely beneficial. It seems that USDA is being somewhat reactive (delayed response) to updated favorable weather.

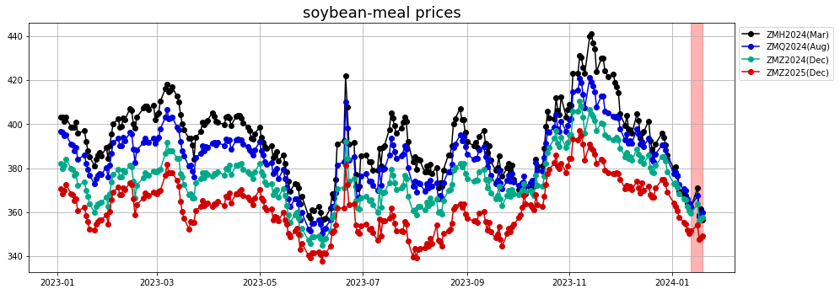

- Soybean meal: Soybean meal remained under intense pressure. Positioning of Managed Money is now net bearish. The last time it was at that level in January was back in 2018 and 2019, when the soybean complex was very bearish with the quota wars.

Forecast has been fairly flat. Latest trajectory is flat for the coming weeks.

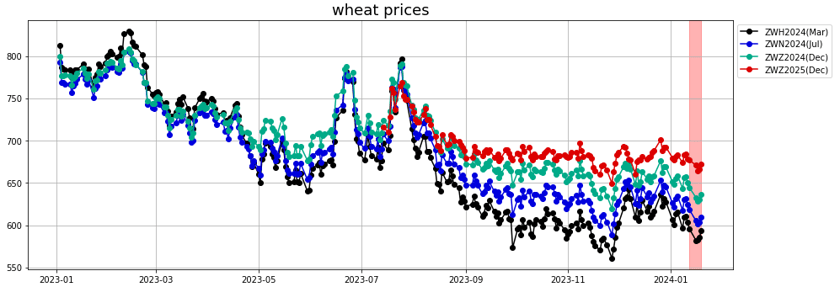

- Wheat: Winter wheat planting came below all estimates in USDA January 12 update. All varieties planting was estimated at 34.425 millions acres, vs 36.699 in 2023, and trade estimates around 35.786. While somewhat supportive, this supply update was not enough to change the downward momentum on wheat.

The USDA net export sales publication on January19 was quite supportive for wheat with about 0.7 MMT

Vegoils

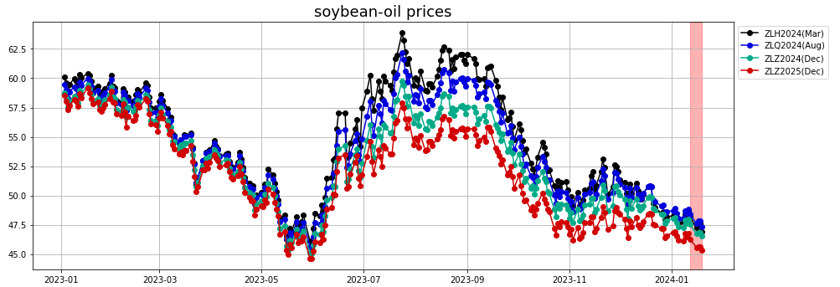

- Soybean oil: soybean oil remained under pressure like the soybean complex. On January 16, NOPA published their update December 2023, showing the highest level of soybean crush of the last six years (and probably the highest ever). At the same time, the soybean oil yield came down and soybean oil inventories, as reported by NOPA, remain lower than in the last five years.

Forecasts had been bullish for the last week or so and did not anticipate this move down.

- Palm oil: Malaysian palm oil futures rose on Thursday, buoyed by robust demand from key buyer China and firmer crude oil prices, although mixed demand from top importer India capped the gains. Good demand from China ahead of the Lunar New Year festive period was seen, but some importers in India opted for soft oils like soya due to disparities in the world's biggest importer of vegetable oil, said Mitesh Saiya, trading manager at Mumbai-based trading firm Kantilal Laxmichand & Co.

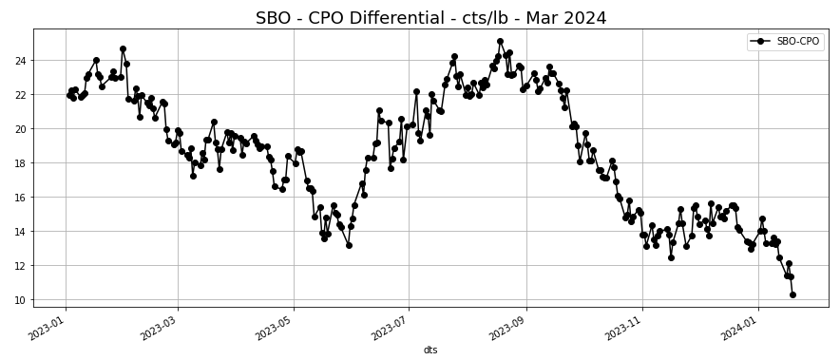

It is worth mentioning that the SBO-CPO differential is reaching new lows in favor of soybean oil.

The forecast had been bullish last week and this move was in line with the Descartes Labs forecast. Further support is expected until the end of the month.

Softs

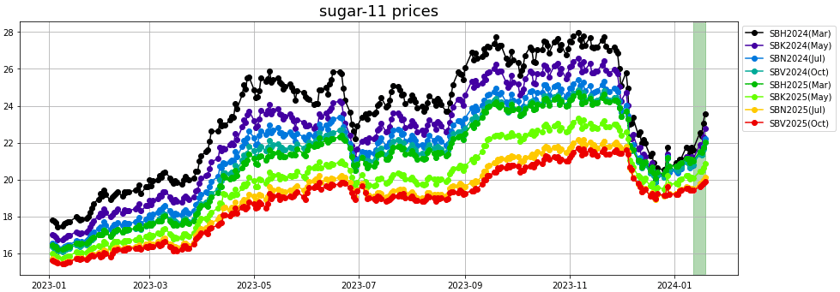

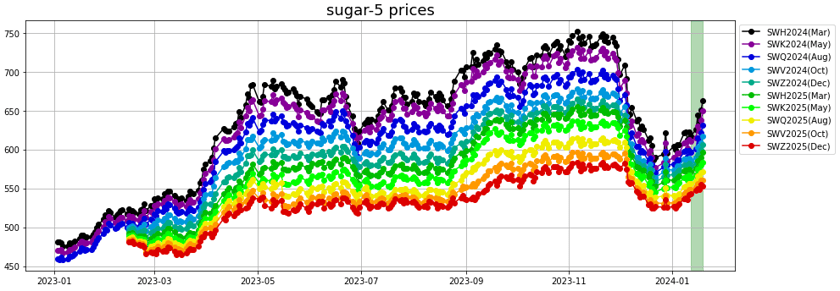

- Sugar: Raw sugar: Sugar prices on Thursday rallied to 1-1/4 month highs and settled sharply higher. Sugar prices are seeing support from concern that the current El Nino weather pattern will curtail global sugar output. Sugar prices are also seeing support from signs that India's ban on sugar exports will be maintained and keep global supplies tight after India announced a 50% export tax on molasses from sugar refining. That reduced the likelihood that India will lift its sugar export curbs in the foreseeable future.

Sugar prices have recently been undercut by higher Brazilian sugar production. Last Thursday, Unica reported Brazil's Center-South sugar output jumped +35.6% y/y in the second half of December to 236,000 MT and that sugar output in the 2023/24 crop year through December rose +25.4% y/y to 42.053 MMT. Meanwhile, Brazil exported 3.7 MMT of sugar in November, marking a new record for the month.

While the overall trajectory since mid December 2023 has been very much in line with the forecasted trajectory back a month ago, recently the model had been bearish and did not anticipate this rally. Forecast is bearish for now until a rebound mid-February.

White sugar: Indian mills' sugar production between October 1 and December 31 was down 7.6% from a year earlier, a leading industry body said. The Thai Sugar Millers Corp on November 1 projected that Thailand's 2023/24 sugar production would fall by -36% y/y to a 17-year low of 7 MMT due to a severe drought. So far this year, rainfall in Thailand is well below the same period last year, and the current El Nino weather system could further reduce precipitation over the next two years.

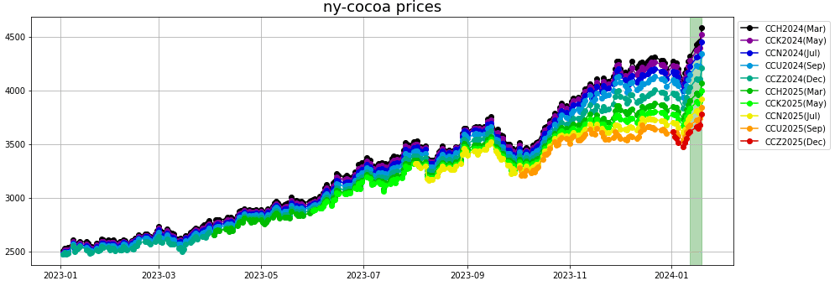

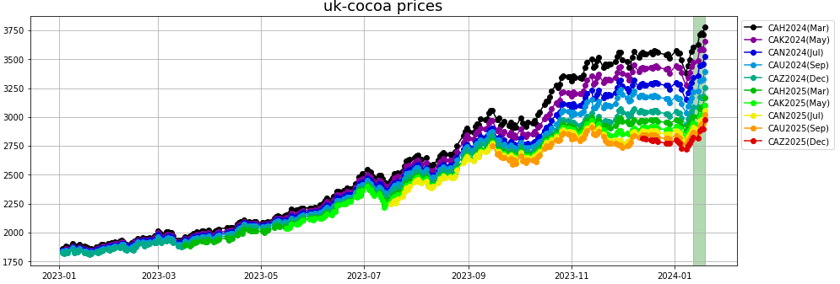

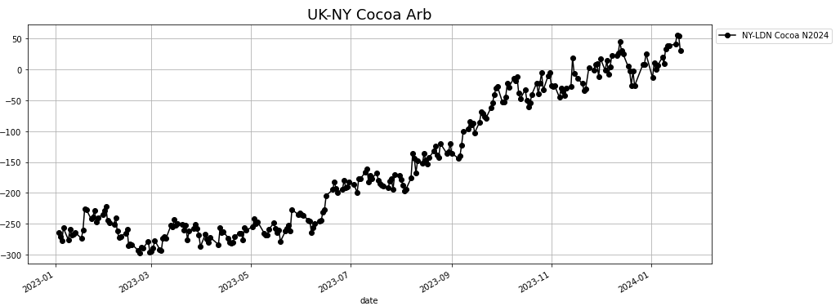

- Cocoa: Cocoa prices on Thursday opened lower but recovered from their worst levels and settled mixed, with NY cocoa posting a 46-year nearest-futures high. Concerns that near-record cocoa prices are starting to curb global demand initially knocked cocoa prices lower Thursday after the Cocoa Association of Asia reported Asian Q4 cocoa grindings fell -8.5% y/y to 211,202 MT. Also, the European Cocoa Association reported that European Q4 cocoa grindings fell -2.5% y/y to 350,739 MT.

However, cocoa prices recovered Thursday, with NY cocoa posting a 46-year high as global supplies remain tight. The Ivory Coast government reported Tuesday that Ivory Coast farmers shipped 911,0890 MT of cocoa to ports from October 1 to January 14, down -37% from the same time last year.

Forecast had been moderately bullish for London cocoa. Latest move was stronger than anticipated and the forecast trajectory is now bearish.

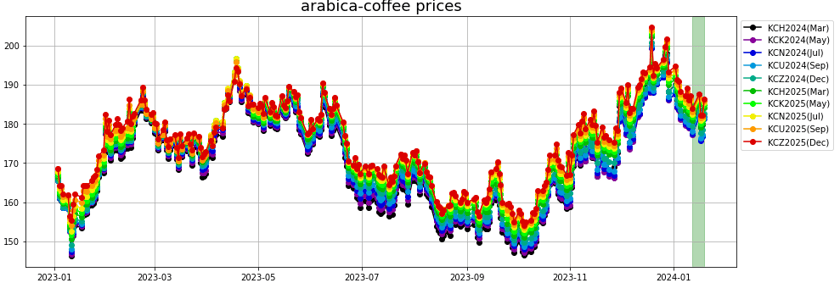

- Coffee: Arabica: Coffee prices rose Friday on concern that recent dry weather in Brazil will damage coffee crops. Somar Meteorologia reported Monday that Brazil's Minas Gerais region received 70.9 mm of rainfall in the past week, or 85% of the historical average. Minas Gerais accounts for about 30% of Brazil's arabica crop.

Descartes Labs model: The model had been moderately bullish over the last week or so and expects the rebound to continue toward 180 cts/lb for Jul024 by end of the month.

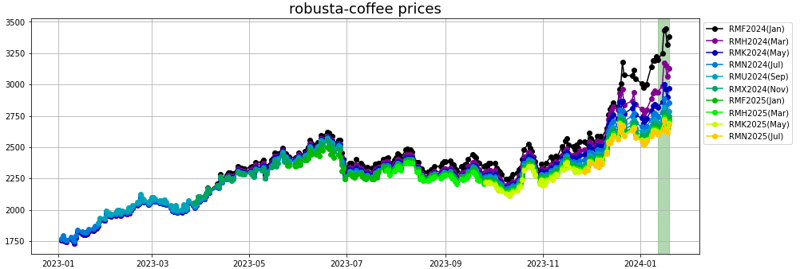

Robusta: On Friday, ICE-monitored robusta coffee inventories fell to a record low of 3,001 lots.

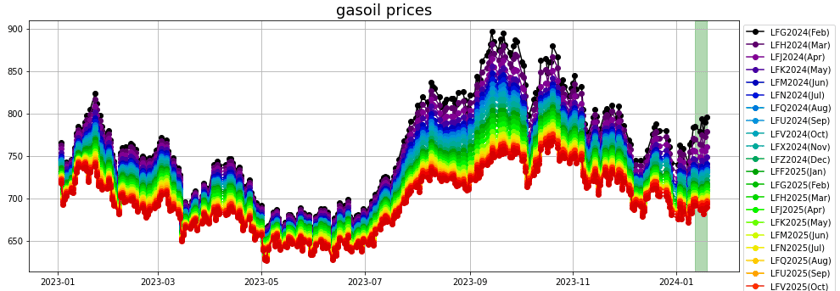

Energy

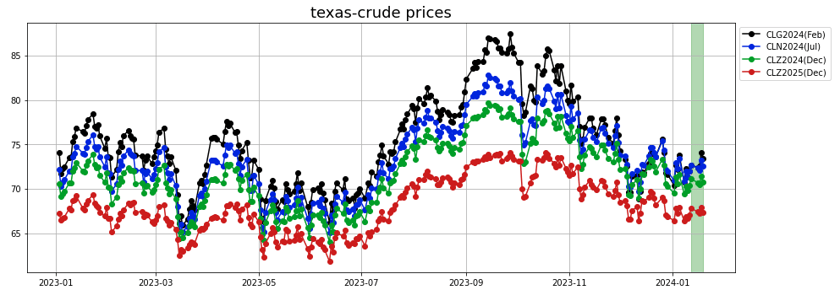

- Crude oil: A cold snap in the US impacting negatively crude production due to freeze-offs, plus a bullish storage number on Thursday, and increased tensions in the Red Sea with more ships attacked by Houthi rockets, supported the market.

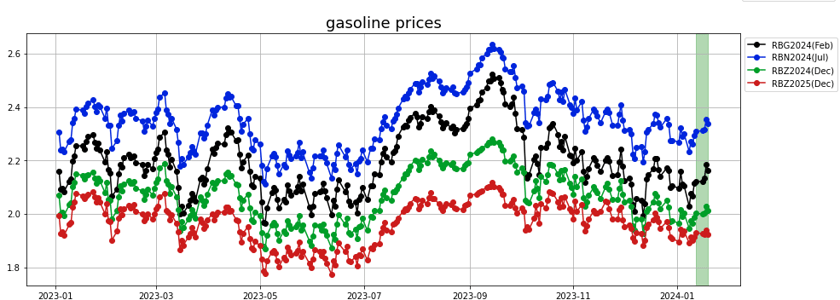

- Gasoline: We again saw some builds in gasoline inventories reported by EIA on Thursday, putting some pressure on the prompt contracts while summer gasoline was supported.

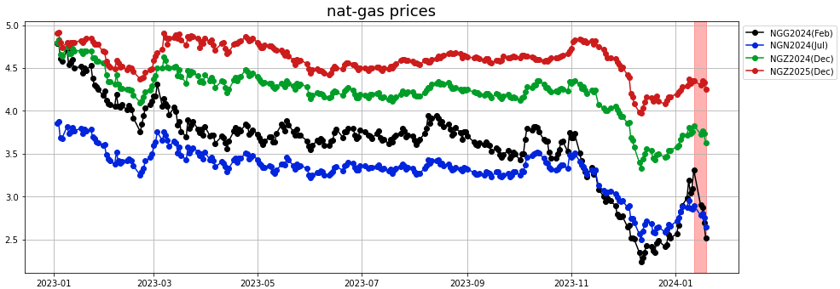

- Natural gas: As the intensity, and especially duration of the cold front, especially in the deep south and in the Northeast, the rally in natural gas did not last very long. Lack of cold and expectation of a warmer than normal early February pressured the market with prices returning quickly towards 2.5 $/MMBtu for February.

Receive Market Report Notifications

Receive Market Report Notifications

Sign up below to get alerts directly in your inbox when a new Market Report is released.