Market Insights Overview: Descartes Labs' advanced geospatial insights uses quantitative models for the most accurate price forecasting, and involves a rigorous process from a broad library of forecasts in agriculture/industrial production, weather and human activity. In this blog, we provide you insights on the current week's market.

*Disclaimer: This blog post and related information is provided by Descartes Labs, Inc. (“Descartes Labs”) and was prepared solely for informational purposes. It is based upon or derived from information generally believed to be reliable, but no representation is made that it is accurate or complete. Descartes Labs accepts no liability with regard to the use of or reliance on it, and it should not be taken as investment, trading, or other advice.

Macro

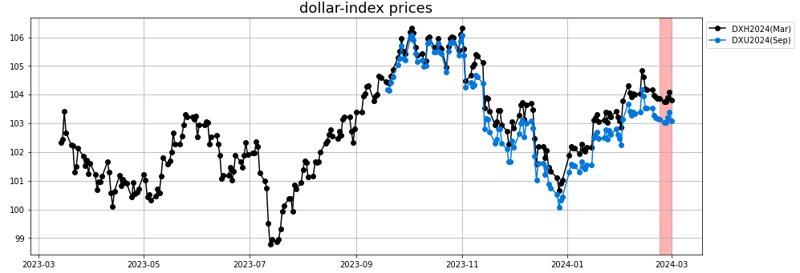

- The dollar retreated from a 1-1/2 week high Friday and posted moderate losses on weaker-than-expected U.S. economic news on Feb ISM manufacturing, Jan construction spending, and the University of Michigan U.S. Feb consumer sentiment.

- The U.S. Feb ISM manufacturing index unexpectedly fell -1.3 to 47.8, weaker than expectations of an increase to 49.5.

- U.S. Jan construction spending unexpectedly fell -0.2% m/m, weaker than expectations of +0.2% m/m and the biggest decline in 15 months.

- The University of Michigan U.S. Feb consumer sentiment index was revised downward by -2.7 to 76.9, weaker than expectations of no change at 79.6.

- Atlanta Fed President Bostic said the Fed needs to hold interest rates higher for longer, so inflation recedes further and it won't have to go back and raise rates again.

- As a result, the markets are discounting the chances for a -25 bp rate cut at 5% for the March 19-20 FOMC meeting and 30% for the following meeting on April 30-May 1.

Grains

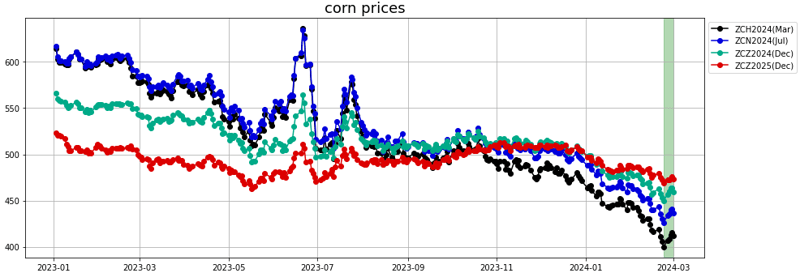

There were no major statistics released over the last couple of weeks. The weaker dollar could have provided some supportive backdrop for the row-crops markets.

- Corn: Corn rebounded from the lows last week. The US exports and sales numbers were noticeable with a strong export number showing an acceleration vs the previous weeks and volumes so far this marketing year accumulating higher than last year at the same time.

The move we observed over last week was in line with the supportive Descartes Labs forecast from last week. Forecast trajectory is moderately bullish with a rally back to 450-475 cts/bu possible.

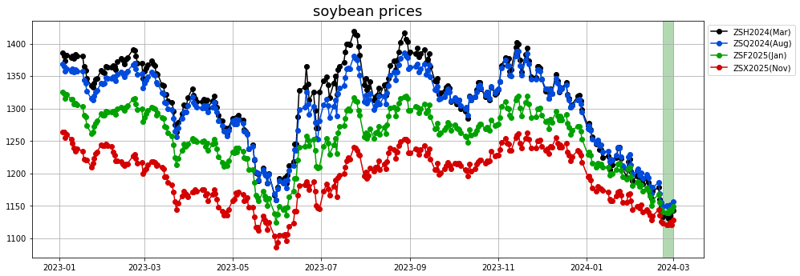

- Soybean: The soybean market dropped to its weakest since November 2020 at $11.28-1/2 a bushel on Thursday before rallying into the end of the week. Chicago Board of Trade soybean futures dipped on Thursday to a new three-year low, pressured by improving South American weather, tepid U.S. export sales and heavier-than-expected contract deliveries, traders said.

In terms of fundamental news, The Buenos Aires grains exchange on Thursday left its forecasts unchanged for the 2023/24 corn and soybean harvest, halting a series of cuts in its estimates as recent rains provided relief to crops. The grains exchange kept at 52.5 million metric tons its forecast for the soybean harvest, while corn estimates remained at 56.5 million tons.

Another update from Industry association Abiove cut its estimate for Brazil's 2024 soybean output for the second time this month to 153.8 million metric tons due to adverse weather.

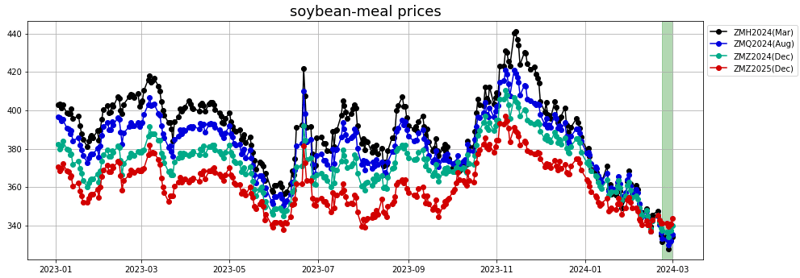

- Soybean meal: CFTC numbers on Thursday showed that commodity funds were net buyers of soybean meal contracts. Soybean meal was further supported by US exports and sales numbers showing an uptick in the sales commitment for the current marketing year.

DL Forecast has been bullish over the last few days capturing some of the late week rally. Forecast trajectory has switched bearish short-term with a potential trough to 320 $/ST before rebounding into April.

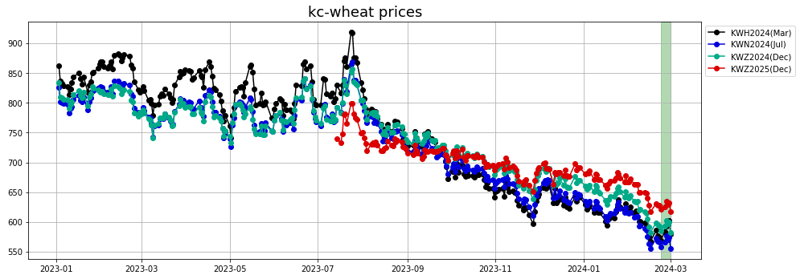

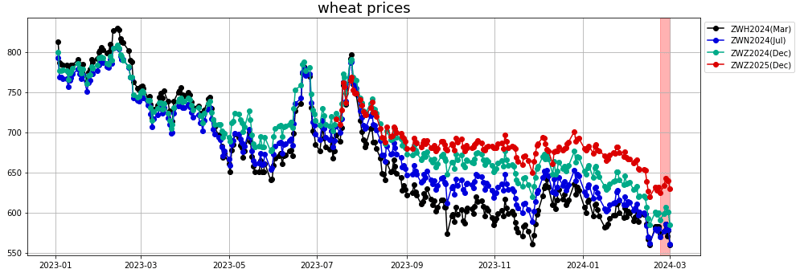

- Wheat: After hitting new lows early in the week, short-covering by speculative investors had helped grain markets bounce off lows, but plentiful supply in the Americas and the Black Sea region is likely to keep a lid on prices. Even the weaker dollar on Friday did not help prevent wheat contracts from moving back down on Friday to their lowest level this year so far.

Vegoils

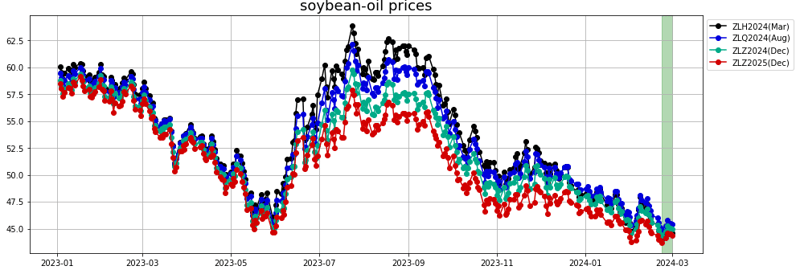

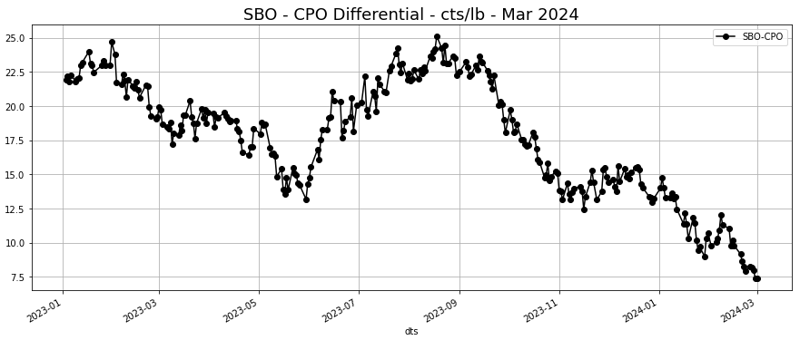

- Soybean oil: Soybean oil markets remained weak although they did rebound a little last week in sympathy with the rest of the oil-seeds sector, supported by palm oil. The SBO-CPO differential has been getting even tighter and is now only 7.5 cts/lb equivalent.

Forecasts had been bullish for the last week or so. The forward picture is showing some further support in the coming days.

- Palm oil: Malaysian palm oil futures closed last week on a strong note, with April-24 contract breaching the 4,000 ringgit mark, tracking strength in rival oils, while the market is waiting for leads from a major industry conference due to be held in Kuala Lumpur next week.

Exports of Malaysian palm oil products for February fell 14.0% to 1,106,054 metric tons from 1,286,509 metric tons shipped during January according to cargo surveyor Intertek Testing Services.

Indonesia's palm oil output this year is expected to rise by 5% year-on-year to 57.6 million tons, while export is expected to stagnate at 32 million to 33 million tons, the Indonesia Palm Oil Association said on Feb 27th.

Softs

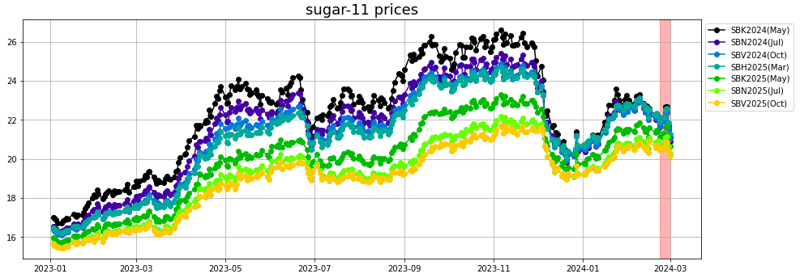

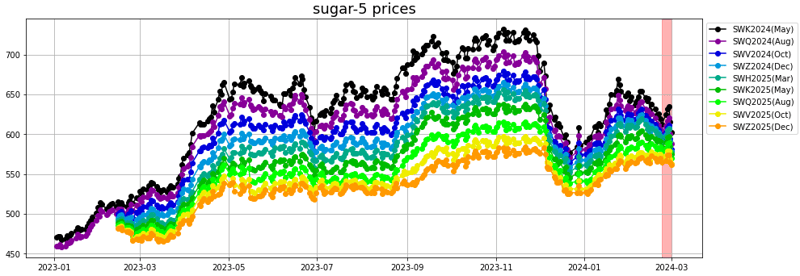

- Sugar: Raw & White sugar: It was quite a volatile week for sugar. After a rally mid-week into the expiration of the March-24 contract, the March contract dropped 6% and May-24 dropped 4.5% and 2.8% on Thursday and Friday respectively.

Dealers said that some traders seemed to have changed their minds about the amount of sugar they were willing to receive, one reason for the large sell-off in the session. Deliveries against the March contract were seen at 25,751 lots, or around 1.3 million metric tons, according to preliminary information from traders, with Wilmar seen as the largest deliverer.

Forecast for sugar #11 had been flat to bearish over last week although such a level of weakness was not anticipated. The outlook is still bearish from here.

White sugar: Talk that India's crop could be slightly larger than expected contributed to the decline in prices and has prompted some to expect a global surplus in the 2023/24 season. On the other hand, Sucden predicted that India's 2024/25 sugar production would fall -15.3% y/y to 28 MMT.

The International Sugar Organization (ISO) more than doubled its 2023/24 global sugar deficit estimate to -689,000 MT from a November estimate of -335,000 MT.

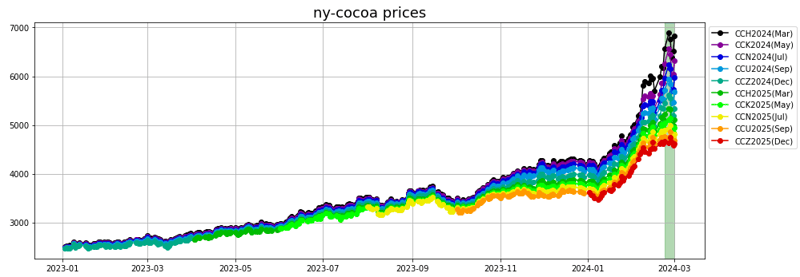

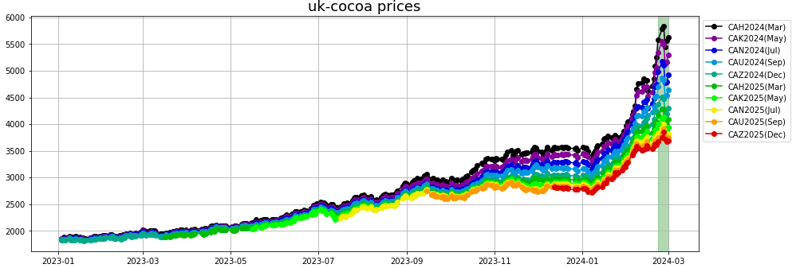

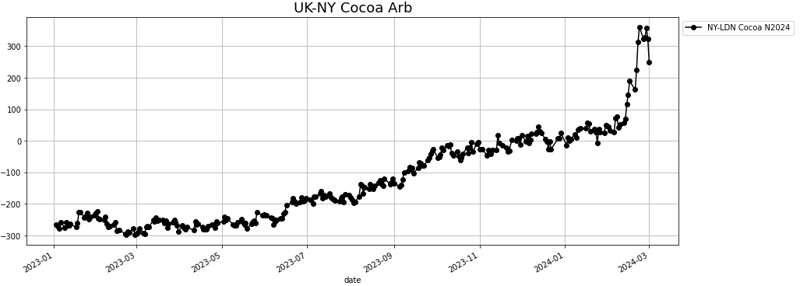

- Cocoa: May London cocoa settled up the week at 5,300 pounds a metric ton although prices remained well below a record high of 5,605 pounds set on Monday.

Dealers said the market had suffered an expected setback after climbing by more than 50% in one month but fundamentals remain supportive following poor crops in Ivory Coast and Ghana, the world's top two producers. The International Cocoa Organization on Thursday forecast an increased global cocoa deficit in the current 2023/24 season as aged trees and disease contribute to a drop in production in top growers Ivory Coast and Ghana.

Forecast had been bearish as of last week. The correction following the new all-time highs on Monday is expecting to continue.

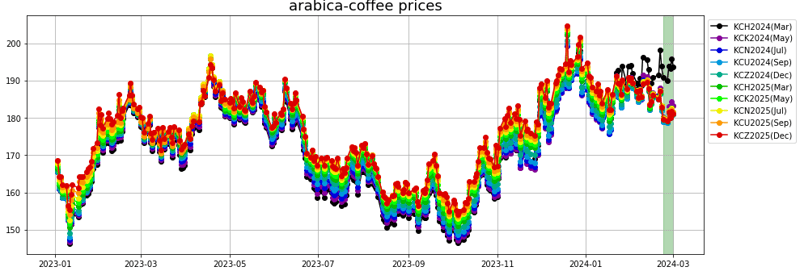

- Coffee: Arabica: There was a large increase in the amount of arabica coffee that is waiting for the evaluation of ICE exchange graders to be added to ICE's certified arabica stocks, according to a report released late on Tuesday.

ICE said in the report that there are 166,027 bags of arabica coffee pending grading at its certified exchanges, of which 133,568 bags come from top grower Brazil.

If a large part of the pending volume is approved, it could lift the overall certified stocks considerably from the current amount of 333,771 bags, which has been gradually rising since it hit a 25-year low of around 220,000 bags seen in November.

Approvals, however, have been low. Tuesday's report said that only 974 bags were approved of a total of 6,672 bags evaluated by ICE graders.

Arabica was under pressure relative to Robusta after Honduras, the biggest coffee producer in Central America reported its Feb coffee exports rose +26% y/y to 932,678 bags.

DL model: Forecast has been slightly bullish for the past week. The outlook is flat.

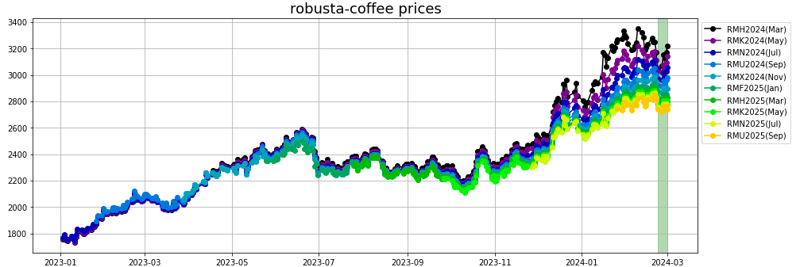

Robusta: Robusta coffee has carryover support from Thursday when Vietnam's General Statistics Office reported that Vietnam's Feb coffee exports fell -20 % y/y to 160,000 MT.

Energy

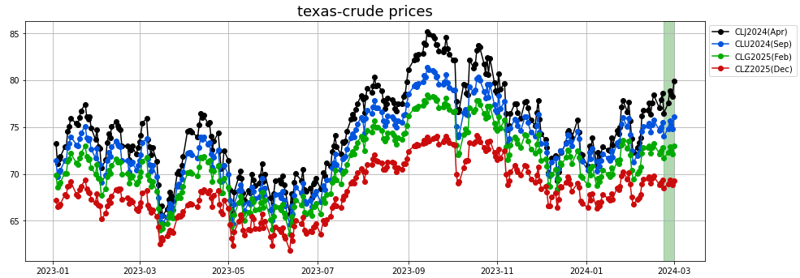

- Crude oil: Despite inventories built reported by EIA, the prompt contracts of WTI were very supported, with Apr-24 settling just shy of 80 $/bbl and prompt calendar spreads widening further.

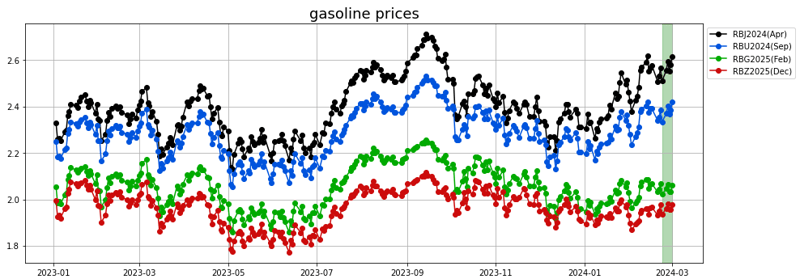

- Gasoline: Stocks for gasoline continued to draw seasonally albeit not as strongly as the previous weeks and benefited mostly from the support in crude.

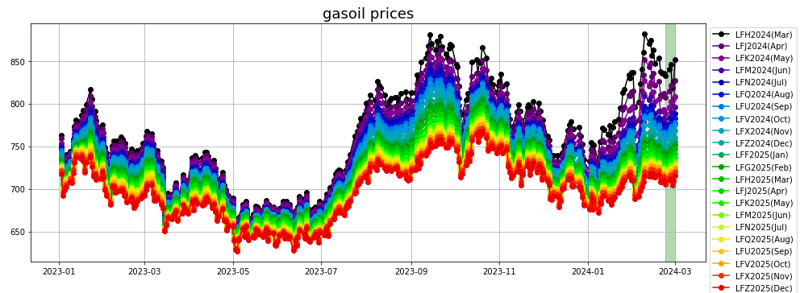

- Diesel/Gasoil: Diesel has underperformed gasoline over the last couple of weeks as the lack of demand from heating reduced the risk premium in the complex. Situation remains relatively tight for now though with low imports in the US and relatively low production on lower runs and switch to jet production.

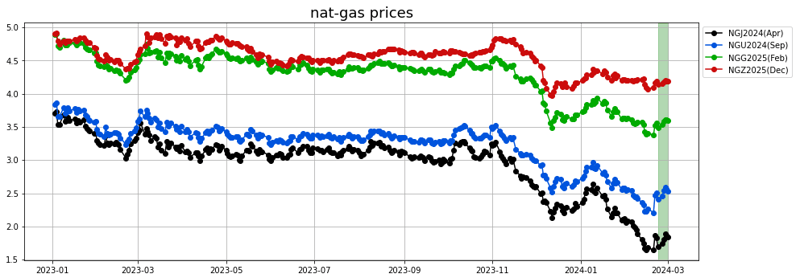

- Natural gas: We saw quite a bit of a rebound over the last two weeks in natural gas. Unexpected drop in production, after the market hit 1.5 $/mmbtu two weeks ago gets the market speculating that we are seeing unannounced economic shut-ins because of the low prices.

Receive Market Report Notifications

Receive Market Report Notifications

Sign up below to get alerts directly in your inbox when a new Market Report is released.