Market Insights Overview: Descartes Labs' advanced geospatial insights uses quantitative models for the most accurate price forecasting, and involves a rigorous process from a broad library of forecasts in agriculture/industrial production, weather and human activity. In this blog, we provide you insights on the current week's market.

*Disclaimer: This blog post and related information is provided by Descartes Labs, Inc. (“Descartes Labs”) and was prepared solely for informational purposes. It is based upon or derived from information generally believed to be reliable, but no representation is made that it is accurate or complete. Descartes Labs accepts no liability with regard to the use of or reliance on it, and it should not be taken as investment, trading, or other advice.

Macro

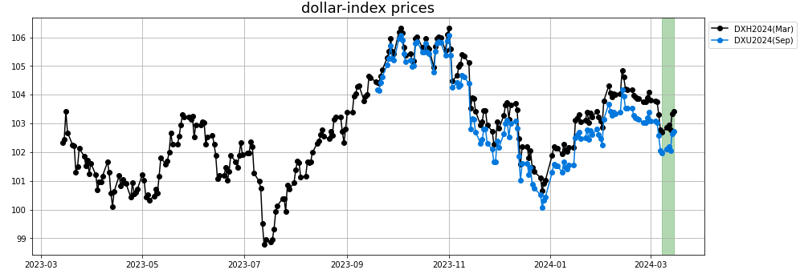

- After initially a quiet week, the dollar rebounded at the end of last week supported by hawkish US Feb import price index ex-petroleum and Feb manufacturing production reports.

- Gains in the dollar were limited after the US Mar Empire manufacturing survey of general business conditions index fell more than expected, and the University of Michigan US Mar consumer sentiment index unexpectedly declined.

- US Feb manufacturing production rose +0.8% m/m, stronger than expectations of +0.3% m/m and the biggest increase in 10 months.

- The US Mar Empire manufacturing survey of general business conditions index fell -18.5 to -20.9, weaker than expectations of -7.0.

- The University of Michigan US Mar consumer sentiment index unexpectedly fell -0.4 to 76.5, weaker than expectations of an increase to 79.7.

- The markets are discounting the chances for a -25 bp rate cut at 1% for next week’s March 19-20 FOMC meeting, 11% for the following meeting on April 30-May 1, and 64% for the meeting after that on June 11-12.

Grains

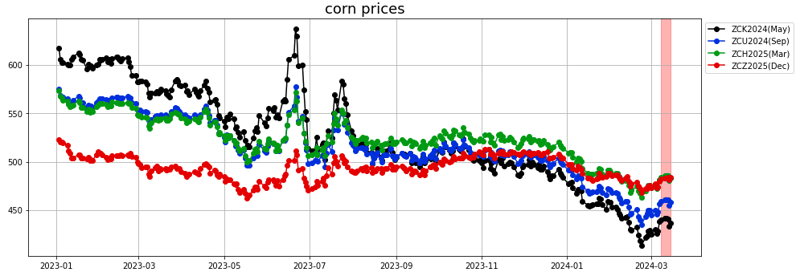

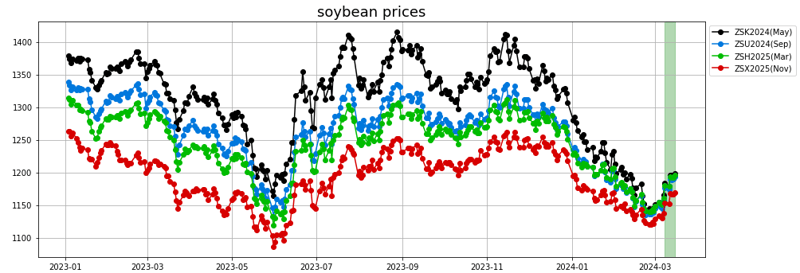

The USDA WASDE was published on March 8th. The March WASDE is usually not a game changer as the updates are usually small and limited. CONAB released their March update on March 12th.

- Corn: US Corn ending stocks were left unchanged in the March WASDE while the trade average was expecting a small decline. USDA adjusted up from 55 to 56 MMT Argentina corn production but kept Brazil constant. In its release, CONAB dialed down its corn production number by about 1 MMT and Brazil ending stocks reduced.

Descartes Labs forecast had been moderately supportive since early March. The outlook is for a moderately upward trajectory into April-24.

- Soybean: Updates from USDA on Mar 8th were limited for soybeans as they left US ending stocks constant and only reduced their estimates for Brazil 23/24 production to 155 MMT and kept Argentina constant at 50 MMT. This contrasts with the CONAB update on Mar 12th, where they reduce further their soybean production estimates to 146.85 MMT, a 2.55 MMT cut and now 8.15 MMT under USDA. That came via a 220k harvested acre increase and a 0.93 bpa yield hit nationally.

AgRural estimates Brazilian harvest is 55% complete, slightly ahead of the 53% from last year.

Prices last week were supported by the announcement that forward sales to unknown destinations were switched to China but the actual net exports number at 0.376 MMT was in the low part of the expected range.

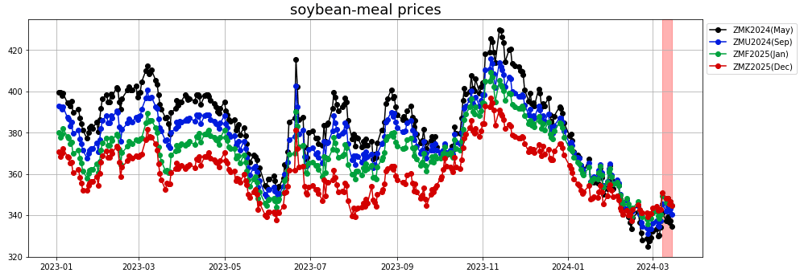

- Soybean meal: CFTC numbers show that funds sold CBOT soymeal in the week ended March 5, marking their most bearish ever start to March (~50k f&o net short). Funds have been net sellers in meal 14 of the last 15 weeks.

Forecast has been bearish since Mar 8th, anticipating a possible retracement towards 320 $/MT.

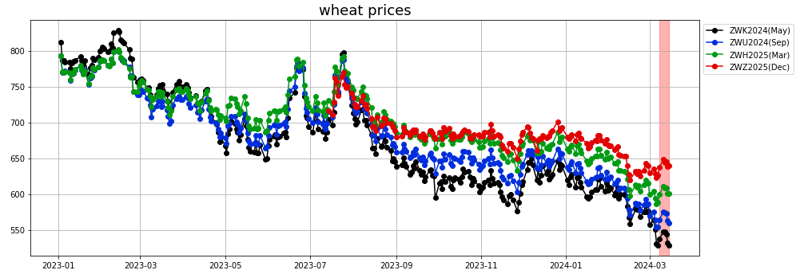

- Wheat: Wheat futures are on track for a third weekly decline, under pressure from Chinese buyers canceling shipments of more than 500,000 tons of U.S. wheat and canceling and postponing over one million tons of Australian wheat amid low Black Sea price.

U.S. wheat exports have struggled amid ample global supplies, including from an expected bumper crop in top exporter Russia.

Russia's IKAR agricultural consultancy said it expects the country's 2024/25 wheat crop to clock in at 93 million tons, up from 91.6 million tons in 2023/24, Russian news agency Interfax reported on Thursday.

On March 8th, the USDA raised US ending stocks due to an export reduction to 0.673 Bn bu while World ending stocks were seen lower 258.8 MMT.

Vegoils

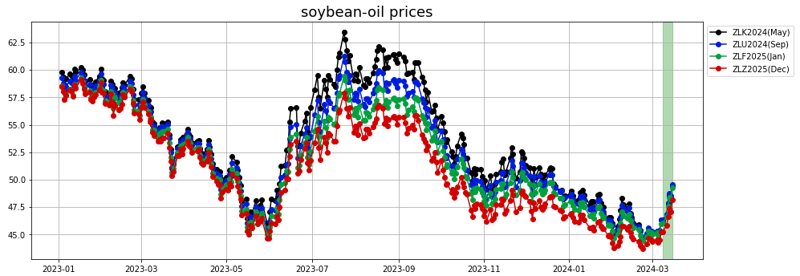

- Soybean oil: Traders are looking for NOPA members to confirm between 170.2 mbu and 185.5 mbu of soybeans were processed in February. The actual data release beat this estimate, reporting a monthly record for month of February at 186..194 Mln bu, a 12.6% YoY growth.

Survey respondents are also looking for soy oil stocks to increase 5.6% for the month to 1.59 billion lbs. The actual number was 1.69 bln lbs, quite a strong MoM increase but still last year by 6.6%.

Forecasts had been bullish since March 8th. The forecast trajectory is still upward sloping but much less aggressively. Descartes Labs sees a potential continuation of the rally up to 52 cts/lb by mid April.

- Palm oil: Malaysian palm oil futures were little changed on Friday, after logging their highest close in more than a year in the previous session, as stronger Dalian rival oils offset weaker crude oil prices.

Malaysia's palm oil stocks at the end of February dwindled to their lowest in seven months as production hit a 10-month low, offsetting the slowdown in exports.

Palm oil prices were supported by stronger price in soybean oil at the Dalian exchange as well. It is possible that the delay in application of some aspects of the EU-DR regarding palm oil and vegetable oils after the lobbying of Indonesia and Malaysia helped support prices as well.

Softs

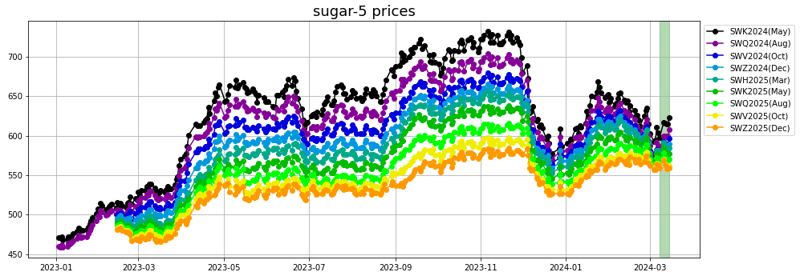

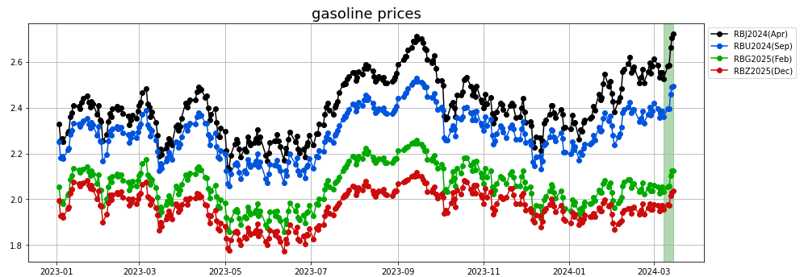

- Sugar: Raw & White sugar: Sugar prices on Friday settled moderately higher, with London sugar posting a 2-week high. Sugar prices gained support from Friday's rally in gasoline prices (RBJ24) to a 5-3/4 month high, which extended this week's gasoline rally to about 20 cents/gallon. The strength in gasoline prices is bullish for ethanol prices and may prompt the world's sugar mills to divert more cane crushing toward ethanol production instead of sugar, thus reducing sugar supplies.

Unica reported Tuesday that Brazil's Center-South sugar output in the second half of February was 16,000 MT, up from zero in the year-earlier period. Also, Brazilian sugar output so far in the 2023-24 marketing year rose +26% y/y to 42.181 MMT. Unica also said it expects 28 mills in the Center-South region to resume production in the first half of March after their off-season pause, which would be more than the year-earlier figure of 10 reopening mills in that period.

Forecasts had been mixed over the last week. Initially bearish but bullish at the very end. Last forecast trajectory is bearish short-term into the end of the month of March.

White sugar: On the bearish side for sugar, the Indian Sugar and Bioenergy Manufacturers Association on Wednesday raised its forecast for India's sugarcane production in the 2023-24 marketing year (that began on Oct 1) by +2.9% to 34 MMT from January's forecast of 33.05 MMT. Higher sugarcane production likely means higher refined sugar production, depending on how much of that sugarcane is converted into ethanol.

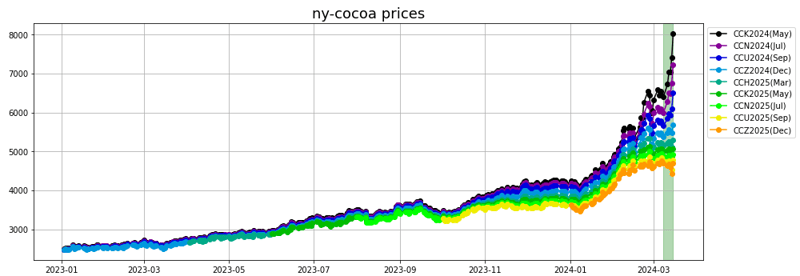

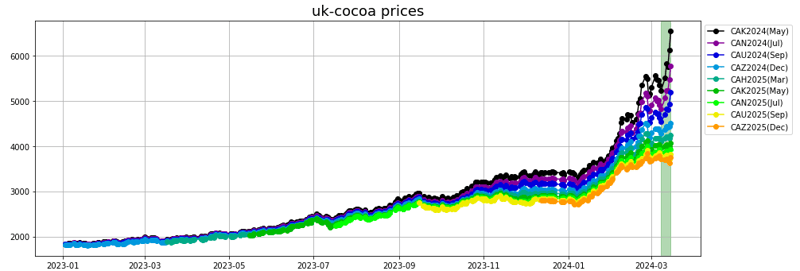

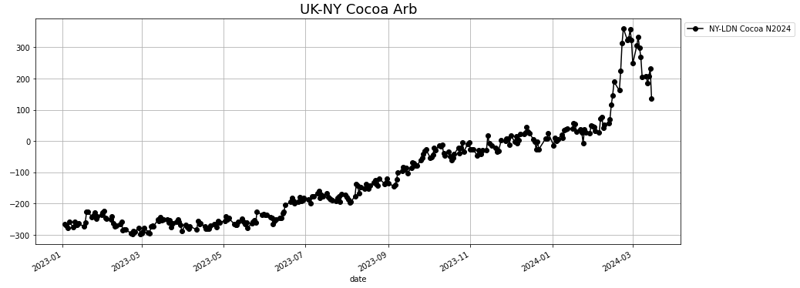

- Cocoa: May-24 New York and London Cocoa rallied even further this past week, clocking a 12-15% increase depending on the contract. Major plants in Ivory Coast and Ghana have stopped or cut processing because they cannot afford to buy beans, four trading sources said, as prices surge after three years of poor harvests, with a fourth expected.

A total of 75,000 metric tons of cocoa was tendered against the ICE March London cocoa contract, which expired on Wednesday, exchange data showed.

Forecaster Maxar said rains should build across Ivory Coast and Ghana through Saturday, which will slow harvesting but improve prospects for the coming crop.

Forecast had been bearish as of last week and did not anticipate such a strong rally.

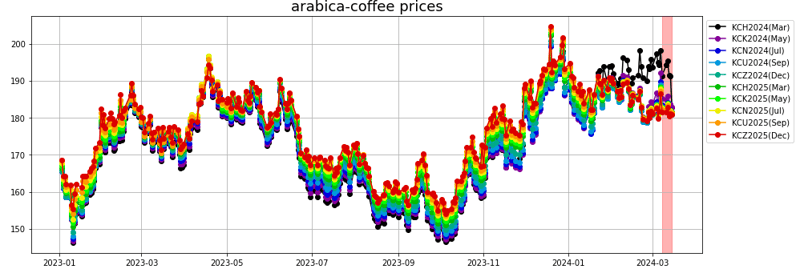

- Coffee: Arabica: Arabica availability in Brazil is said to be tight in the short term until the new crop starts to arrive to the market.

"Whoever is short must bid higher to absorb coffee for the nearby periods, hence diffs remain supported. New crop is a totally different story," said a local broker.

Arabica stocks on the ICE exchange are at their highest since October at 458,107 bags, with more than 170,000 bags pending grading.

DL model: Forecast has been flat for the past week and the outlook remains flat.

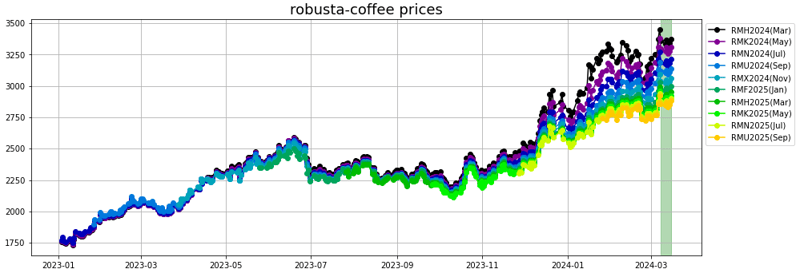

Robusta: Robusta coffee price premiums in top producers Vietnam and Indonesia rose this week as supplies remain tight, with concerns growing over the next crop due to lack of rains this season.

Energy

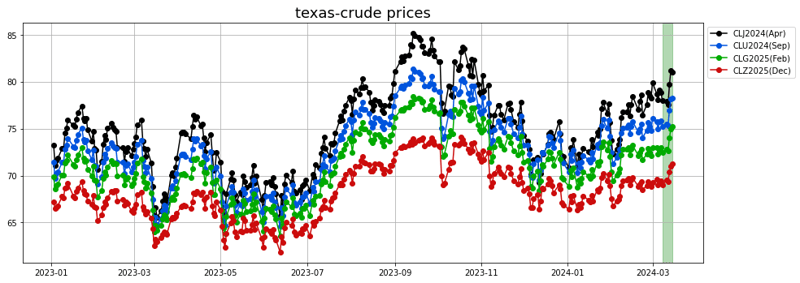

- Crude oil: Oil prices edged lower on Friday but were on track to gain nearly 4% for the week as sharp declines in U.S. crude and fuel inventories, drone strikes on Russian refineries and a rise in energy demand forecasts buoyed prices.

- Gasoline: The EIA reported a stronger than expected inventories draws, despite a growing refineries utilization, hinting at demand picking up.

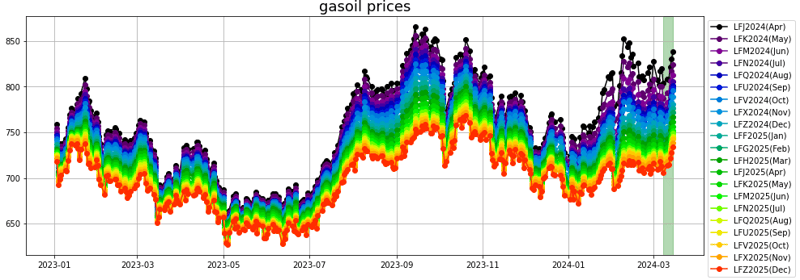

- Diesel/Gasoil: Diesel has underperformed gasoline over the last couple of weeks as the lack of demand from heating reduced the risk premium in the complex. Situation remains relatively tight for now though with low imports in the US and relatively low production on lower runs and switch to jet production.

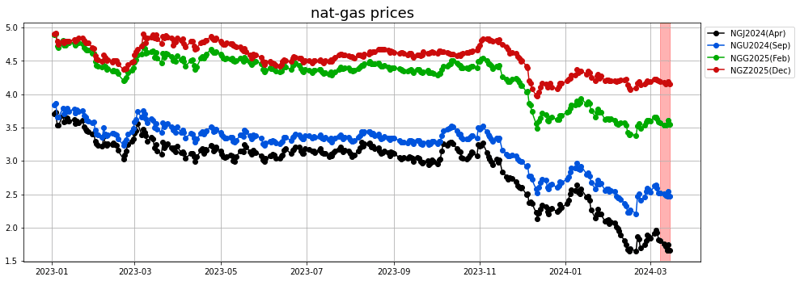

- Natural gas: The rebound was short-lived and price moved down significantly dragged down by cash prices in the physical markets around 1.25 $/mmbtu. In addition, the warmer weather and the maintenance at Freeport LNG terminal had a negative impact on demand recently and this is expected to continue until May.

Receive Market Report Notifications

Receive Market Report Notifications

Sign up below to get alerts directly in your inbox when a new Market Report is released.