Market Insights Overview: Descartes Labs' advanced geospatial insights uses quantitative models for the most accurate price forecasting, and involves a rigorous process from a broad library of forecasts in agriculture/industrial production, weather and human activity. In this blog, we provide you insights on the current week's market.

*Disclaimer: This blog post and related information is provided by Descartes Labs, Inc. (“Descartes Labs”) and was prepared solely for informational purposes. It is based upon or derived from information generally believed to be reliable, but no representation is made that it is accurate or complete. Descartes Labs accepts no liability with regard to the use of or reliance on it, and it should not be taken as investment, trading, or other advice.

Macro

-

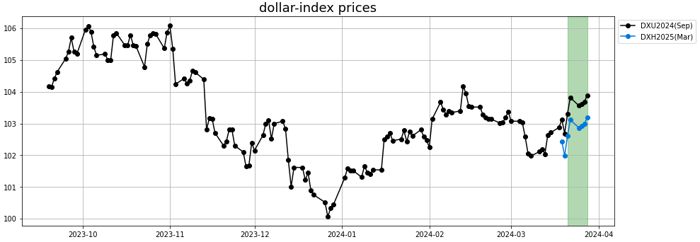

The dollar continued to rally over the past week as reduction in inflation has slowed.

-

Hawkish comments Wednesday night from Fed Governor Waller boosted the dollar when he said there’s “no rush” for the Fed to ease monetary policy: “it is appropriate to reduce the overall number of rate cuts or push them further into the future in response to the recent data.”

-

While the numbers regarding the labor market remain strong, some analysts are getting wary of the recurring downward revisions that are made to recent numbers, suggesting that the situation may be weaker than what we think.

-

The Euro and the yen are facing pressure from a weaker economic backdrop.

Grains

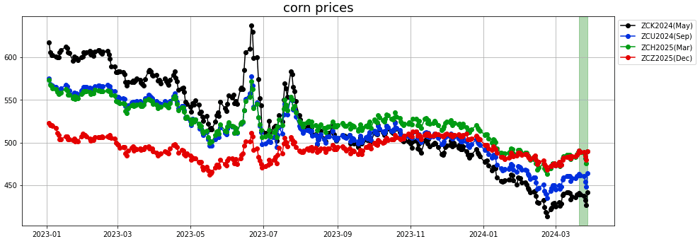

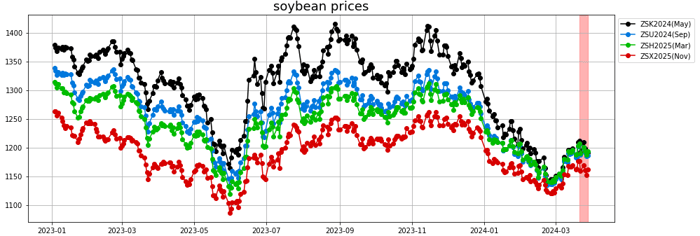

Last week saw the end of the Q1-24 and thus the publications of the first planting intentions for the US and the US Quarterly Grain stocks numbers. It was also a shorter trading week for most products as CME and ICE exchanges were closed on Good Friday.

- Corn: Corn benefited from bullish numbers from both publications. March 1, 2024 US Corn came out at 8.345 billions bushels, which was lower than the trade estimate around 8.427. It still marks a large year-on-year increase from 7.4 Bn bu to 8.35.

Corn planting intentions, in their first release of the season, came out quite bullish for corn, at 90.04 millions acres, marking a -4.9% decrease vs last year. The decline is visible in almost every major production state, especially in the South with states like Arkansas, Mississippi, Texas showing declines as large as 15-25%. We can note that this number was lower than USDA estimates provided during the Ag Outlook Forum back in February 2024.

Descartes Labs forecast had been flat to bearish over last week. The outlook is for a moderately downward trajectory into April-24.

- Soybean: The updates were on the opposite side for soybeans. Not only did the quarterly grain stocks estimates came up above trade expectations at 1.845 billions bushels (+150 Mlns bu year-on-year), but the planting intentions showed a rotation out of corn into soybeans and thus an increase by 3.5% for soybeans acres for 2024, at an estimated 86.5 millions acres. Here again, the expected increase is spread out across all major states with the exception of Kansas. Note that for soybean as well, the planting intentions came out lower than the USDA Ag Outlook estimate.

Not surprisingly, these data releases pressured soybean prices even further into the end of the shortened week.

In Brazil, Consultancy Agroconsult said Brazil would produce 156.5 million metric tons of soybeans this year, increasing its estimate after surveying fields nationally.

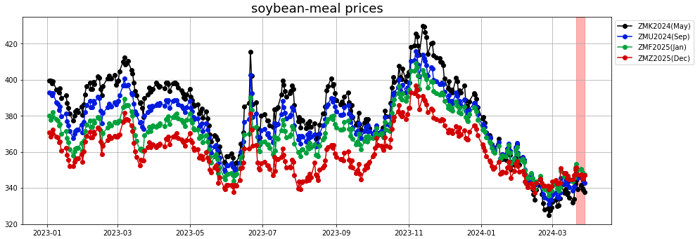

- Soybean meal: There was little news on soybean meal, which price action tracked soybean’s.

Forecast had been bearish over last week and still anticipates a possible retracement towards 320 $/MT

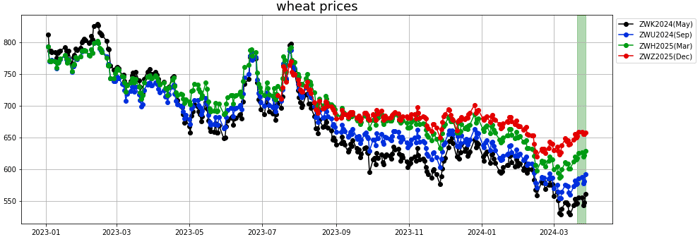

- Wheat: The big news in wheat planting intentions - the large decrease year on year to 47.5 millions acres - was already well telegraphed back in February 2024. Out of the 3 varieties of wheat, winter wheat was the one the most impacted by this decline, seeing a drop by more than 2.5 millions acre, while spring wheat plantings are seen unchanged and durum wheat is actually seeing an increase year on year.

Also creating supply concerns were Russian attacks on infrastructure in Ukraine, another large grain exporter, and Russian accusations that Kyiv helped arrange a terror attack in Moscow, but these worries have faded.

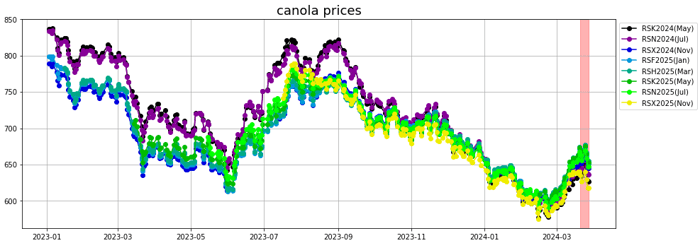

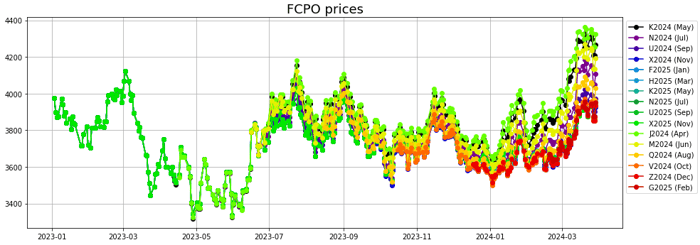

Vegoils

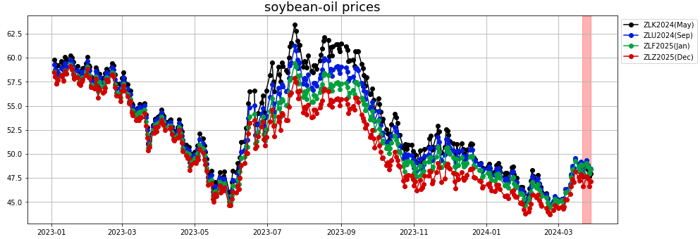

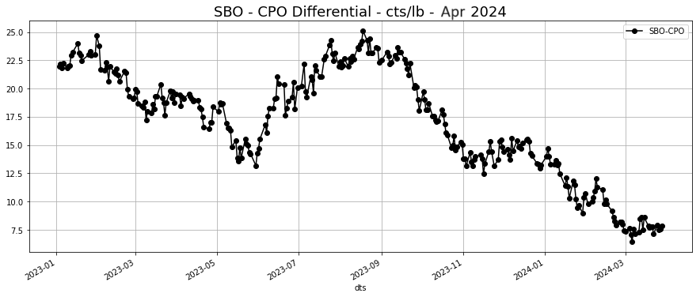

- Soybean oil: The vegetable oil and oilseeds sector was under-pressure after the latest rally.

Forecasts had turned bearish over last week. The outlook trajectory is flat for the coming week or so before a more supportive outlook towards 50 cts/lb by the end of the month.

- Palm oil: Palm oil prices consolidated at the top of the recent price range.

Indonesia aims to double subsidies for palm oil replanting to 60 million rupiah ($3,785.49) per hectare from May to boost farmers' participation, Chief Economic Minister Airlangga Hartarto said on Thursday.

Indonesia's January palm oil exports, including refined products, stood at 2.8 million metric tons, down from 2.95 million tons in the same month last year, data from the Indonesian Palm Oil Association (GAPKI) showed on Thursday. Production of crude palm oil and kernel oil rose to 4.63 million tons from 4.26 million tons, the data showed.

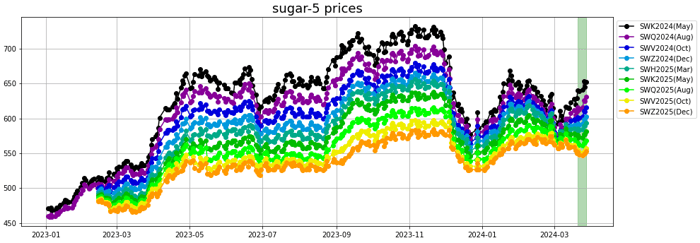

Softs

- Sugar: Raw & White sugar: Sugar prices on Thursday posted moderate gains, with NY sugar rising to a 1-month high and London sugar climbing to a 1-1/2-month high. Thursday's rally in crude prices (CLK24) to a 1-week high was bullish for sugar.

Sugar also had carryover support from Monday when US sugar producers called for reduced sugar imports from Mexico. The American Sugar Coalition called on the US government to lower the amount of sugar Mexico can send to the US by 44%, which would likely boost prices and require the US to purchase sugar from other countries, tapping already tight global sugar supplies.

Forecasts had been shifting slightly bullish mid-last week capturing this late last week move and support this week. Short-term outlook is for further support into next week.

White sugar: Reduced sugar production in India is a bullish factor for prices. The Indian Sugar Mills Association (ISMA) reported last Monday that India's 2023/24 sugar output from Oct through Mar 15 fell -0.7% y/y to 28.1 MMT.

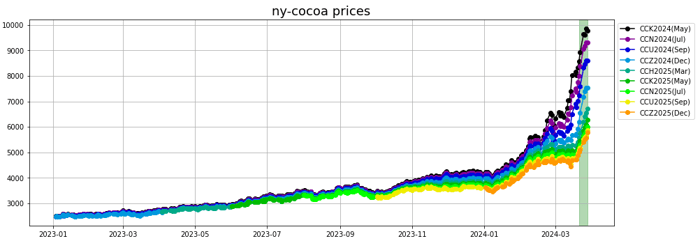

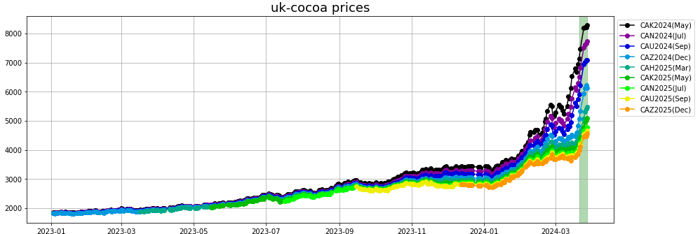

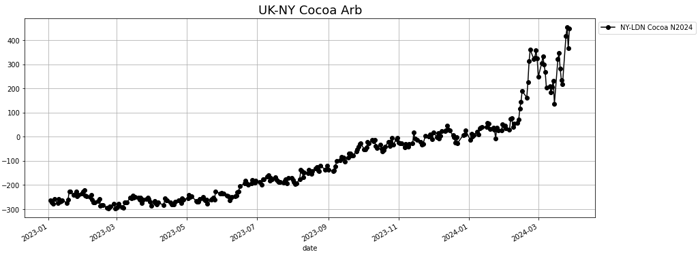

- Cocoa: The rally in cocoa continued last week, with New York cocoa trading above 10,000 $/MT shortly during Wednesday session.

Dealers said the market's focus was turning to the mid-crop in top grower Ivory Coast, which begins next week with a decline to around 400,000 to 500,000 tons expected, down from 600,000 tons a year ago.

"Normally, the mid-crop is less important due to its smaller size. However, given the already weak main crop, it is likely to be more important at this time. If the estimates come down further, this could provide a further boost to the cocoa price," Commerzbank said in a note.

Forecasts had remained bearish as of last week and did not anticipated a continuation of the rally. The outlook is for some consolidation of July-24 contract around 7000 GBP/MT.

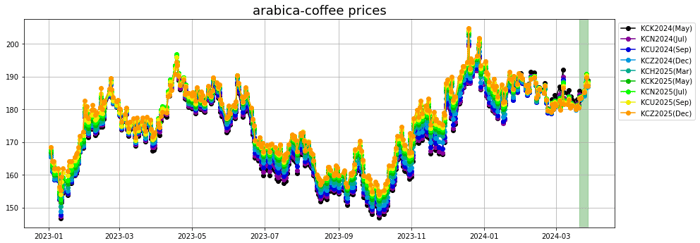

- Coffee: Arabica: Arabica benefited from the overall support in soft commodities as the weather in Brazil was generally favorable and crops appeared to be in good shape.

Forecast has been flat for the past week. With this small rally, the outlook trajectory is bearish on the short-term.

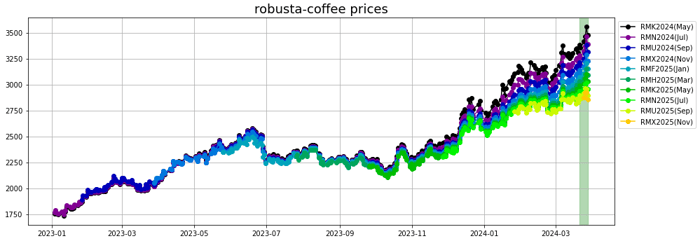

Robusta: The market remained on track for a fifth successive weekly gain. Dealers said supplies were exceptionally tight in Vietnam while there were concerns that dry weather could reduce next year's crop in the world's top robusta producer. Availability of conilon (robusta) coffee in Brazil when the next harvest gets underway in April could alleviate the tightness reflected in prices.

A sharp year-on-year decline in exports from Indonesia has also helped to support prices.

Energy

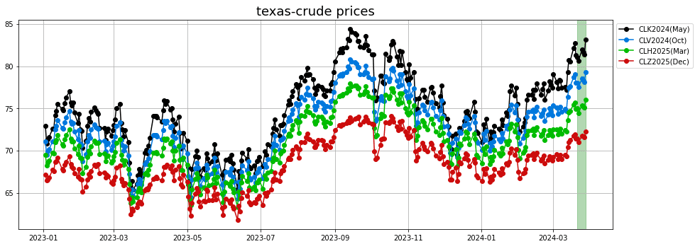

- Crude oil: After a weak start of the week, crude rallied into Thursday as the market expected OPEC+ to stay the course and keep limiting supplies. The EIA data release on Wednesday were less bearish than anticipated and helped to support prices.

Russian potentially cutting production because of its refineries being targeted by drones might have supported prices as well.

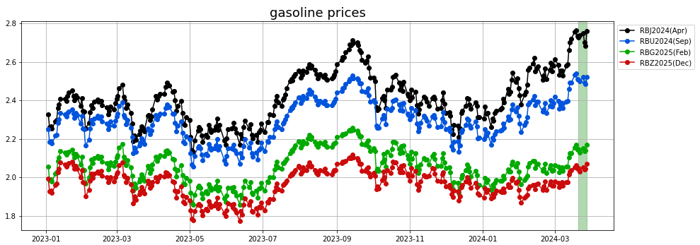

- Gasoline: Despite a weak statistics release on Wednesday which pressured gasoline prices.

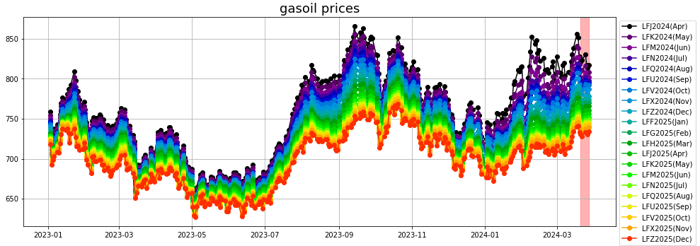

- Diesel/Gasoil: We are seeing quite a rebound in diesel yields. Coupled with higher runs, production is now expected higher at a time when demand is seasonally lower, which should facilitate replenishment of the inventories.

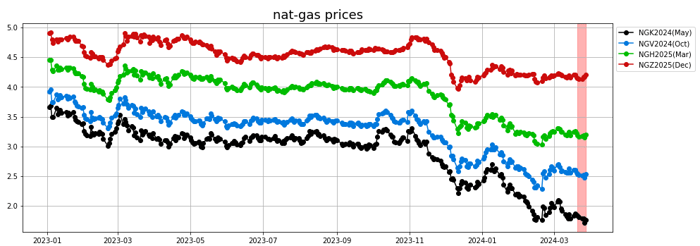

- Natural gas: The natural gas remained plagued by the same issues of large production, some LNG trains currently in maintenance and overall warmer than normal weather.

Receive Market Report Notifications

Receive Market Report Notifications

Sign up below to get alerts directly in your inbox when a new Market Report is released.