Market Insights Overview: Descartes Labs' advanced geospatial insights uses quantitative models for the most accurate price forecasting, and involves a rigorous process from a broad library of forecasts in agriculture/industrial production, weather and human activity. In this blog, we provide you insights on the current week's market.

*Disclaimer: This blog post and related information is provided by Descartes Labs, Inc. (“Descartes Labs”) and was prepared solely for informational purposes. It is based upon or derived from information generally believed to be reliable, but no representation is made that it is accurate or complete. Descartes Labs accepts no liability with regard to the use of or reliance on it, and it should not be taken as investment, trading, or other advice.

Macro

- After a sluggish beginning of the week, the dollar rallied to a 7-week high on Friday following a supportive job report, following the associated jump in yields expectations. The markets are discounting the chances for a -25 bp rate cut at 22% for the March 19-20 FOMC meeting and a 89% chance for that same -25 bp rate cut at the following meeting on April 30-May 1.

- Friday’s U.S. economic news was better than expected and bullish for the dollar. Jan nonfarm payrolls jumped +353,000, stronger than expectations of +185,000 and the biggest increase in a year.

- Also, the Jan unemployment rate was unchanged at 3.7%, showing a stronger labor market than expectations of an increase to 3.8%. In addition, Jan average hourly earnings rose +0.6% m/m and +4.5% y/y, stronger than expectations of +0.3% m/m and +4.1% y/y.

- Finally, the University of Michigan U.S. Jan consumer sentiment index was revised upward by +0.2 to a 2-1/2 year high of 79.0, stronger than expectations of 78.9.

Grains

February WASDE is scheduled for release on Thursday, February 8th.

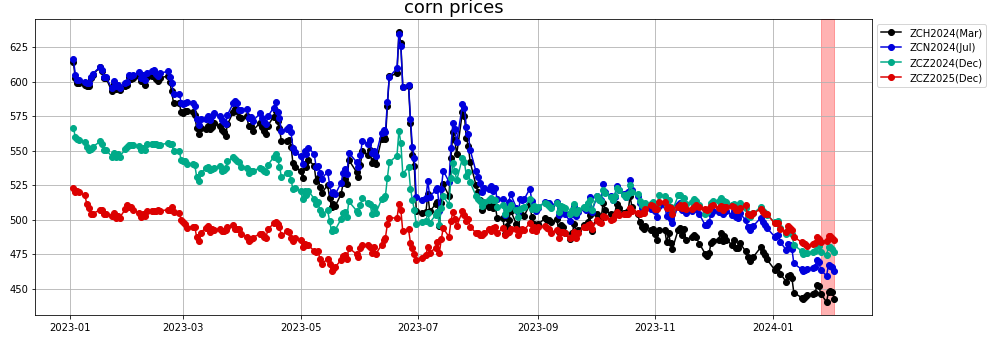

- Corn: CBOT Corn has been near lows not seen since December of 2020 but was up slightly (0.2% on Friday at $4.48 a bushel). The prospect of large harvests in South America and faltering demand in China have hung over grain markets in the new year.

World cereal production in 2023 is expected to reach a record high, the United Nations food agency said on Friday as it reported that its food price index fell to its lowest in almost three years in January.

Reported exports sales were near high-end of expectations though normal for the week.

The DL forecast had been supportive over the last week or so and the rally did not materialize so far. Forecast trajectory is still bullish.

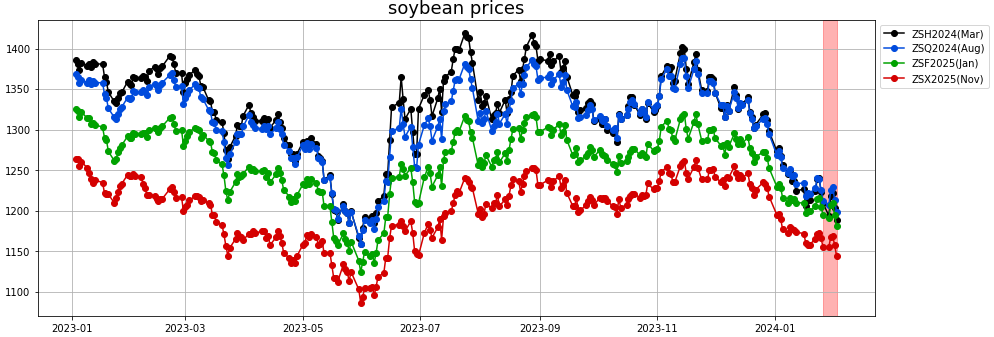

- Soybean:

U.S. export sentiment was dented on Thursday when the U.S. Department of Agriculture (USDA) reported the lowest weekly old-crop U.S. soybean export sales so far this season.

Demand for soybeans from China, by far the largest soy importer, is lackluster because of a shaky economy and a shrinking pig herd.

Demand for US soybeans, proxied by the exports and sales numbers, were at a marketing year low on Thursday report at only 0.165 MMT for WE Jan 25, vs expectations of 0.5-1 MMT

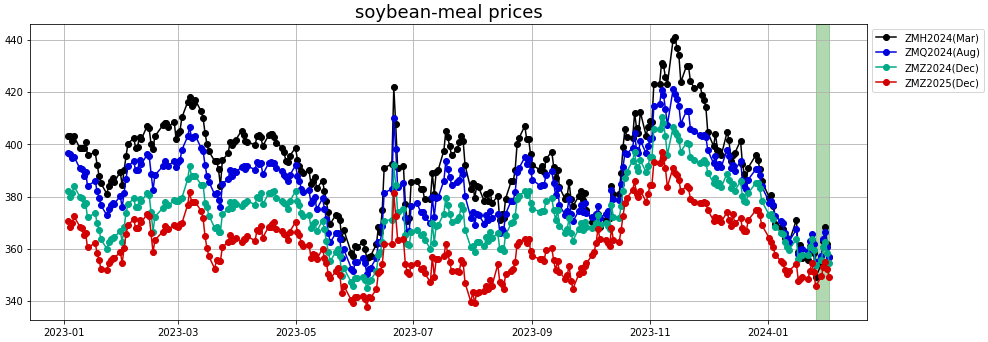

- Soybean meal: Weekly U.S. soymeal export sales last week were the second best in over a year, Philippines was the top buyer. Soybean meal prices were probably helped as well by the heatwave in Argentina that is being monitored for potential impact on developing soy and corn crops, which had previously benefited from abundant rain.

DL Forecast has been bullish over the last week capturing some of the realized rally. Forecast trajectory is still bullish until mid-February.

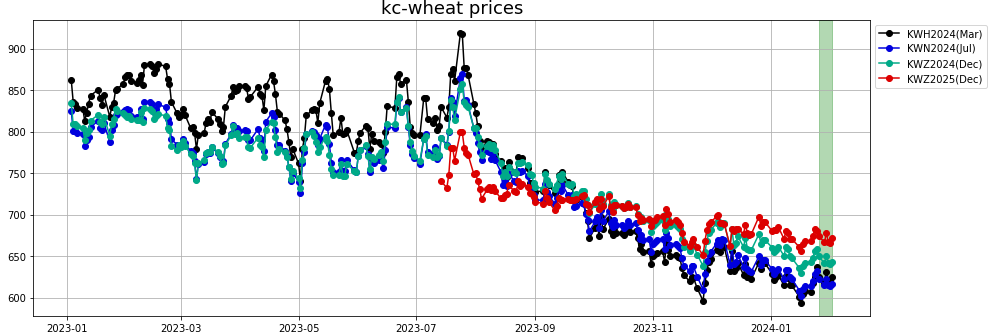

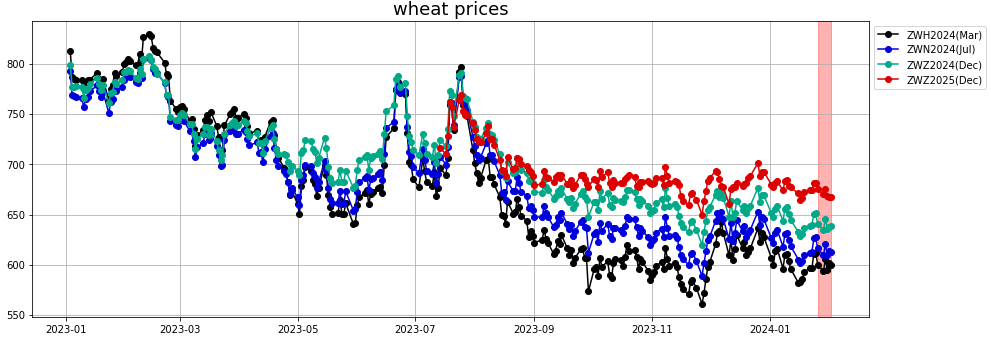

- Wheat: Falling wheat prices in Russia, which still has a large surplus to shift before this summer's harvest, have kept the wheat market's focus on Black Sea supplies.

Russia's agriculture minister, meanwhile, said the country would increase the area for the 2024 harvest by 300,000 hectares to 84.5 million hectares, bolstering expectations for another bumper crop.

Euronext wheat futures hit contract lows. CBOT wheat traded at a three-year low of $5.40 in September.

However, there was unconfirmed talk about fresh Chinese demand for French wheat, which traders said has contributed to a bounce in U.S. and European futures since Thursday.

The European Commission proposed measures to limit agricultural imports from Ukraine and offer greater flexibility on rules for fallow land in a bid to quell protests by angry farmers in France and other EU members.

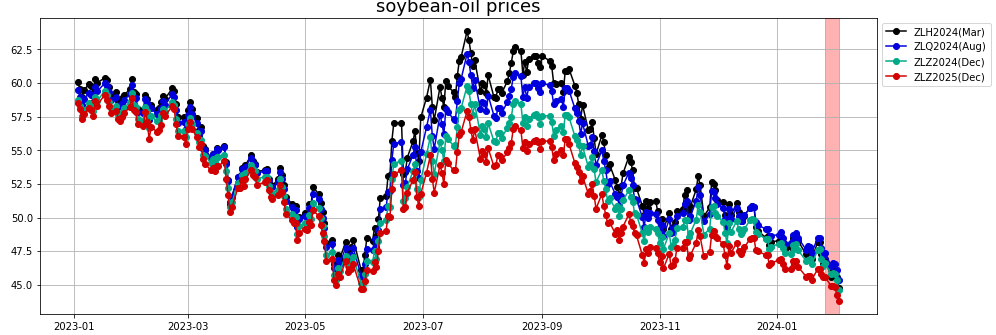

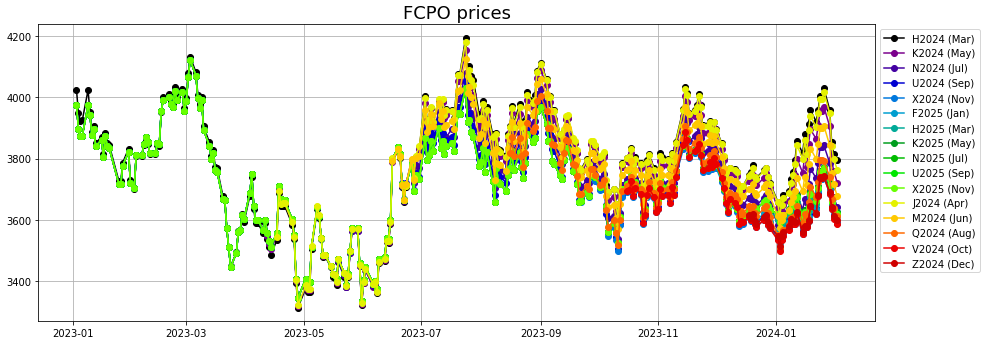

Vegoils

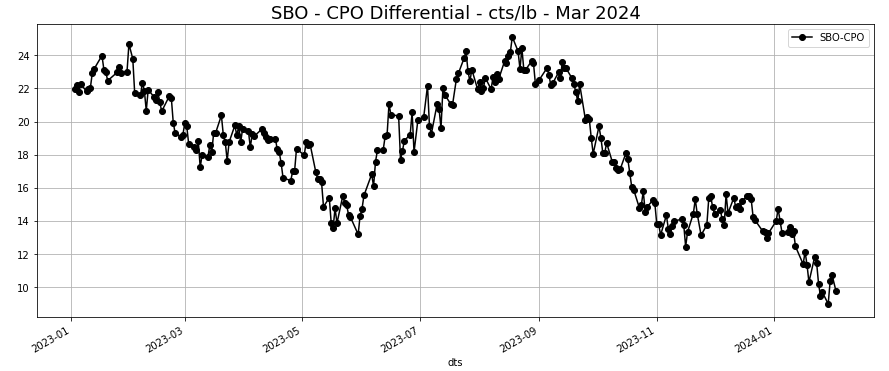

- Soybean oil: Nothing was really supportive for the vegetable oils market as we will see later when talking about crude palm oil.

Forecasts had been bullish for the last week or so and did not anticipate this move down. Still bullish going forward albeit less aggressively.

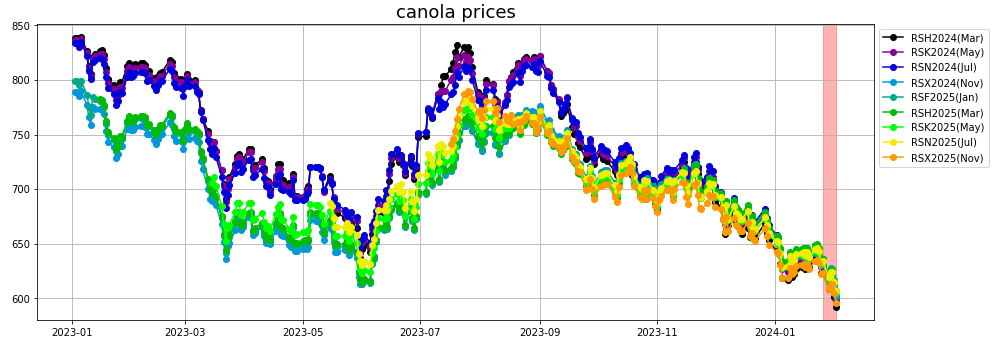

Canola:

- Palm oil: Fears regarding demand from China pressured the market last week.

China's manufacturing activity in January contracted for the fourth straight month, an official factory survey showed.

A liquidation order on property giant China Evergrande Group 3333.HK from a Hong Kong court on Monday dealt a fresh blow to the country's fragile property market, casting a shadow on China's demand outlook. (Caixin survey)

The soft Chinese data also weighed on Brent crude oil prices. Weaker crude prices make palm a less attractive option for biodiesel feedstock.

Exports of Malaysian palm oil products fell 9.4% to 1,227,101 tons in January, independent inspection company AmSpec Agri Malaysia said. Another independent cargo surveyor, Intertek Testing Services, estimated exports fell 6.7% to 1,286,509 tons this month.

India would step up efforts to boost local oilseed production, the finance minister said on Wednesday, as part of plans to cut pricey imports of vegetable oils from the world's top edible oil producers.

"The Lunar Festival buying seems to have concluded, and the focus now shifts to China's economic situation and what they do post festival."

The forecast had been slightly bearish as of a week ago but is now bullish following the sell-off.

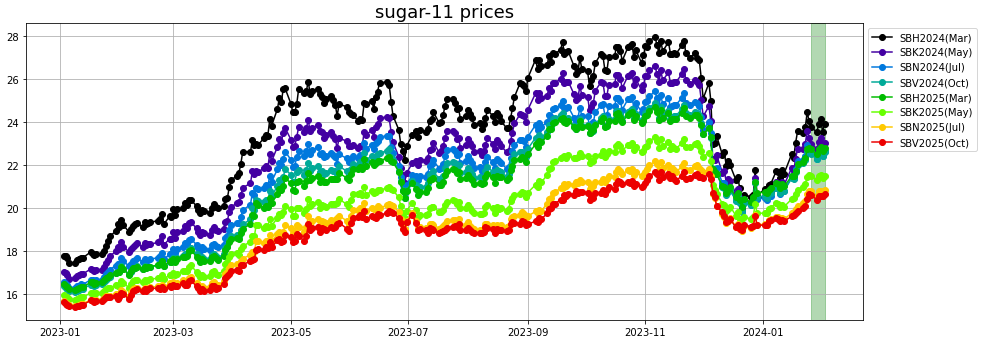

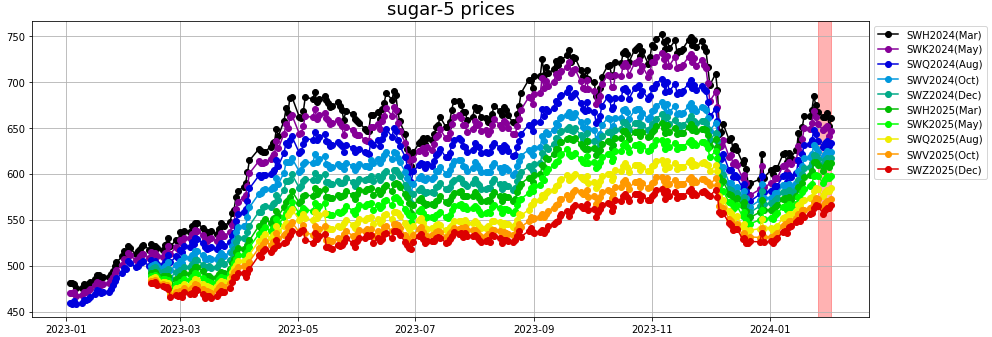

Softs

- Sugar: Raw sugar: Dealers cited uncertainty about Brazil's 2024 crop as rains have been below average.

Broker StoneX on Wednesday projected Brazil's new sugarcane crop at 622 million tons, 5.4% below the previous one.

Forecast for sugar #11 has been bearish over the last couple of weeks and is still expecting weakness going forward. Forecast for sugar #5 had been flattish and is still expecting some supported price on the short-term before a gradual rally back above 700 $/MT.

White sugar: Ukraine's 2023 white beet sugar output jumped to 1.8 million metric tons from around 1 million in 2022, the agriculture ministry said on Thursday, after farmers increased the area sown to sugar beet.

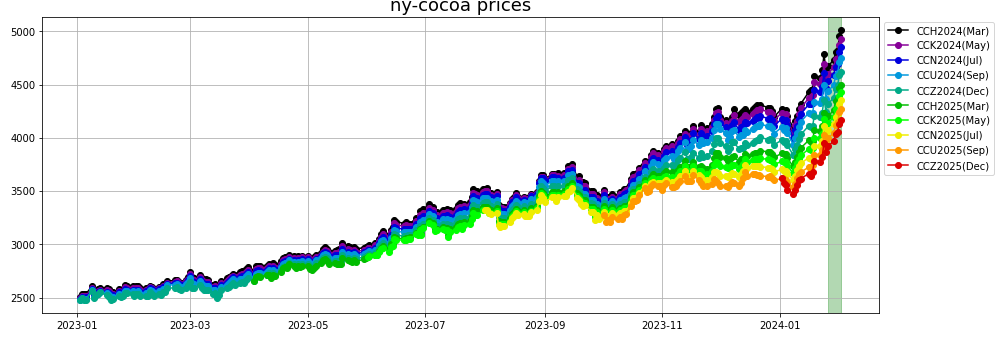

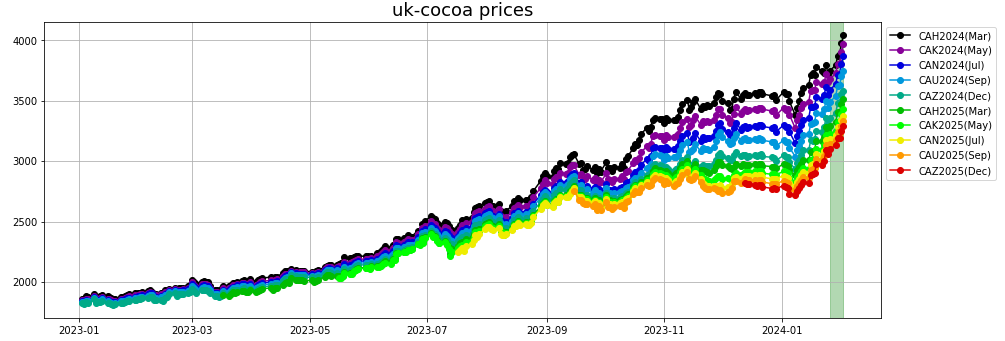

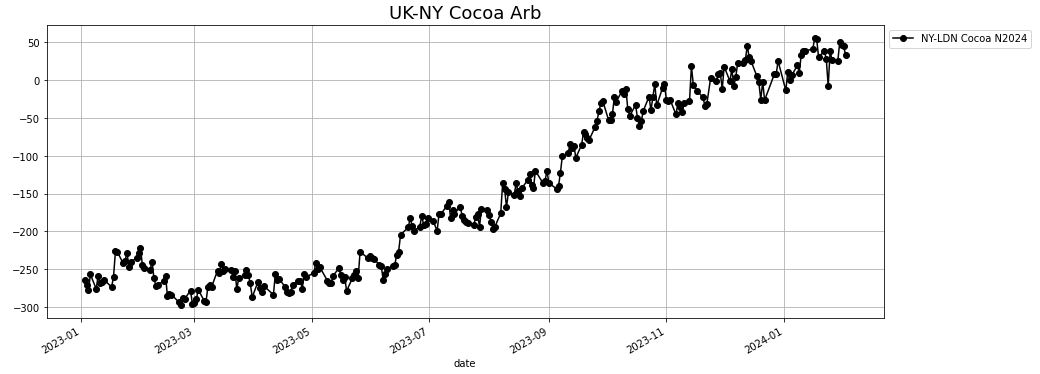

- Cocoa: Dealers noted open interest for London cocoa was continuing to climb, with speculators adding to long positions against the backdrop of supportive fundamentals.

Poor crops in Ivory Coast and Ghana are expected to lead to a large global deficit in the current 2023/24 season.

Amazingly, cocoa rally continued at an even faster price, breaching 5,000 $/MT for New York cocoa, having raised by 20% after the drop early January.

Forecast had been bearish as of last week. Following the latest rally, the forecast trajectory adjusted to be more flattish short-term before weakening during the second half of February.

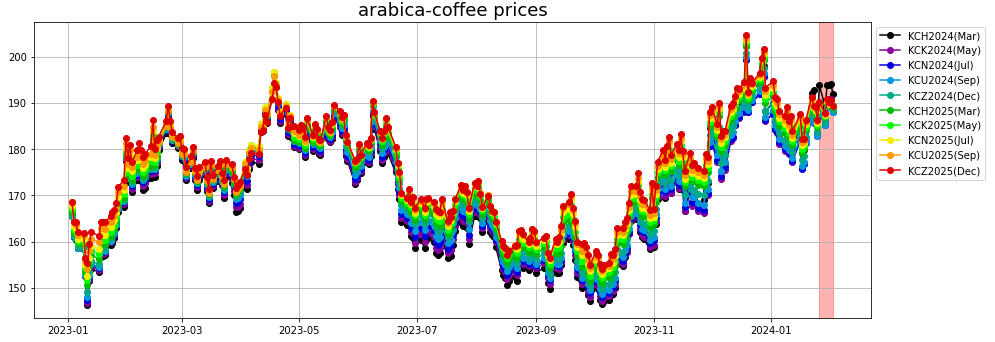

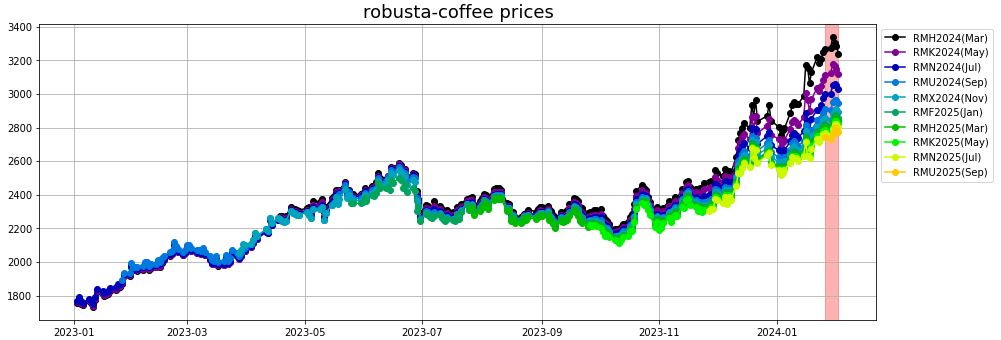

- Coffee: Arabica: Destination stocks were incredibly low when the Red Sea problems began, disrupting the flow of robustas and, to a lower extent, arabicas in Europe," Rabobank said in a note.

Coffee trader Comexim projected the new Brazilian crop at 67.15 million bags, a small increase over the current crop.

DL model: Forecast has been slightly bearish for the past week and is still expecting some slight weakness in February.

Robusta: Dealers said the market had lost some ground after setting a contract high of $3,379 on Tuesday but remained underpinned by supply tightness in Europe partly owing to disruption of the flow of Asian supplies through the Red Sea.

Prices in top robusta grower Vietnam edged up this week though trade was sluggish ahead of the week-long Lunar New Year holiday starting next week.

Green coffee stocks in Japan fell 8% in December to the lowest in seven years.

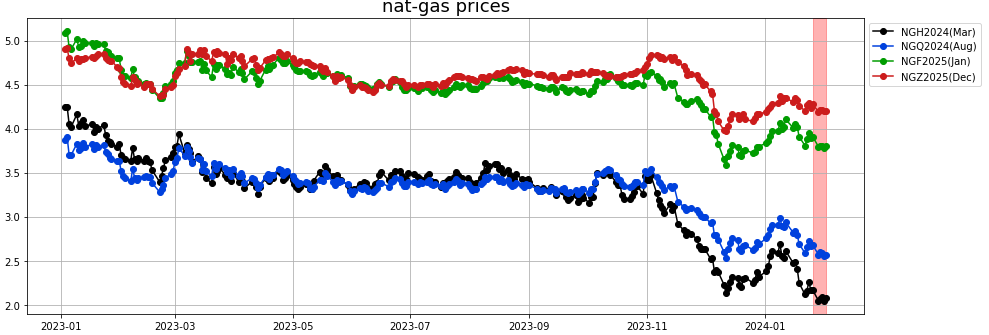

Energy

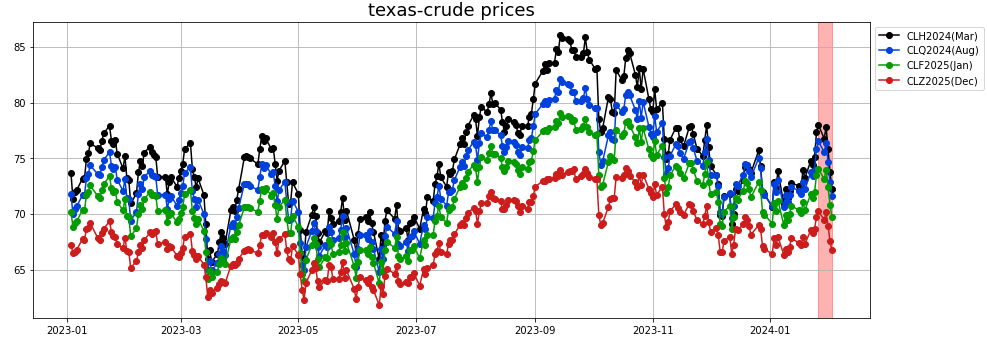

- Crude oil: Sharp decline this week after last week rally. 2 weeks ago, crude market was supported by a series of inventories draws following production freeze-offs and the situation in the Red Sea and the Middle East conflict. Last week, prospect of a cease-fire brokered by Qatar and concerns over China demand, and refineries maintenance season ramping up pressured the market.

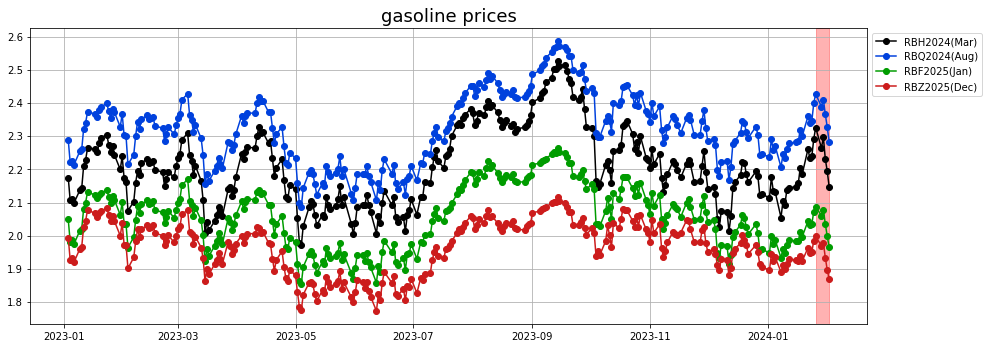

- Gasoline: We again saw some builds in gasoline inventories reported by EIA on Thursday, with a demand still disappointing.

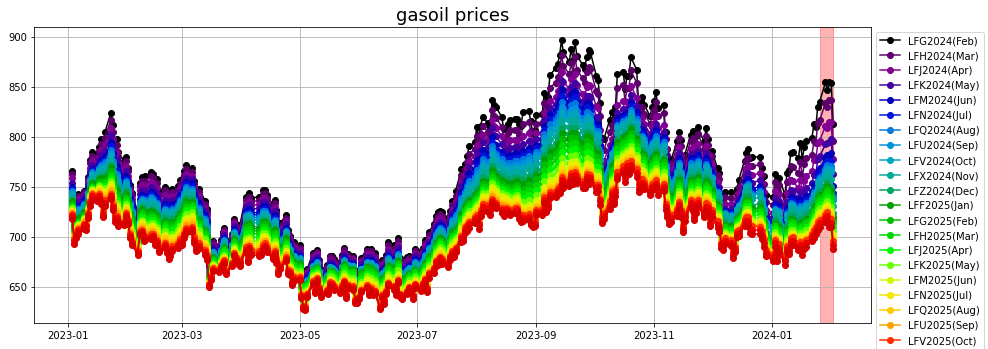

- Diesel/Gasoil: Weakness in diesel was even more pronounced last week, following the events described above.

- Natural gas: We are seeing a continuation of the sell-off in natural gas over the last two weeks as the colder than normal weather expectations have disappeared. Sentiment has also shifted more bearish very long-term following Biden’s administration decision to delay approval on LNG plants planning to start in 2026 and beyond due to environmental impact.

Receive Market Report Notifications

Receive Market Report Notifications

Sign up below to get alerts directly in your inbox when a new Market Report is released.