Market Insights Overview: Descartes Labs' advanced geospatial insights uses quantitative models for the most accurate price forecasting, and involves a rigorous process from a broad library of forecasts in agriculture/industrial production, weather and human activity. In this blog, we provide you insights on the current week's market.

*Disclaimer: This blog post and related information is provided by Descartes Labs, Inc. (“Descartes Labs”) and was prepared solely for informational purposes. It is based upon or derived from information generally believed to be reliable, but no representation is made that it is accurate or complete. Descartes Labs accepts no liability with regard to the use of or reliance on it, and it should not be taken as investment, trading, or other advice.

Macro

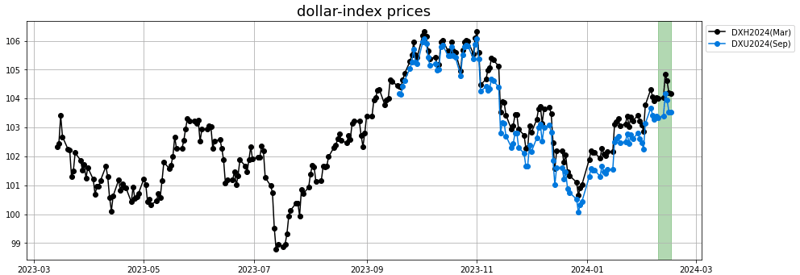

- The dollar closed last week on an up note, closing the 5th week of gains since the beginning of 2024.

- Retail sales falling more than expected in January weighed on the dollar, while the recent unemployment numbers still hint at a tight labor market.

- A string of strong economic data has quashed any lingering expectations of an early and deep rate cut from the Fed, with traders now pricing in an 80% chance of a rate cut in June, according to the CME FedWatch tool. Markets had initially priced in March as the starting point of the Fed's easing cycle. Traders now expect 94 basis points of cuts this year, nearer to Fed's own projection of 75 bps of easing and drastically lower than the 160 bps of cuts markets priced in at the end of 2023.

Grains

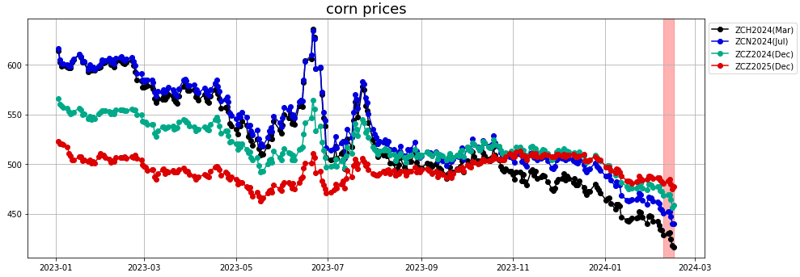

February WASDE was released on Thursday, February 8th. Another large data release was the USDA Grains & Oilseeds outlook on February 15th.

USDA is projecting a net decrease in planted acreage in the US across the main three row crops, from 227.8 million acres in 2023 to 225.5 in 2024. Wheat and Corn acreage would be down ~3 million acres each while soybean acreage could grow by 4 million acres. In any case, USDA is projecting higher ending stocks for corn, wheat and soybeans.

- Corn: In the WASDE, Corn US ending stocks for 23/24 came in at 2.172 billion bushels (for the 2023 crop), above the market expectations of around 2.146 and above the USDA expectations published in January.

The world ending stocks number was more supportive, at 322 MMT, helped by lower estimates for South American corn crop production. USDA revised down their numbers for Argentina and Brazil to 55 MMT and 124 MMT respectively.

The DL forecast had been supportive over the last week and the rally did not materialize so far. Forecast trajectory is still bullish.

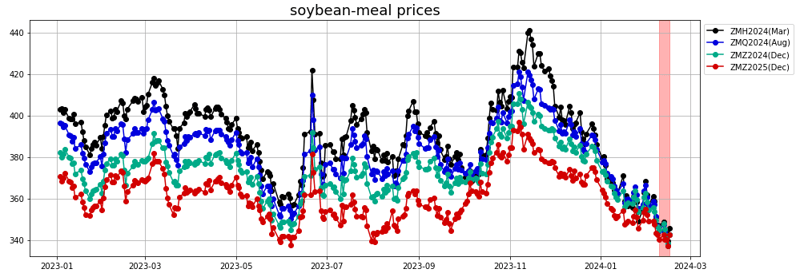

- Soybean: In the WASDE, US ending stocks for the 23/24 marketing year for soybeans were even more disappointing for prices as the estimate came in at 312 million bushels, up from the 280 million estimate back in January. The market had expected the January estimate to hold but this news triggered a sell-off after the publication.

Regarding South America, USDA adjusted Brazil's production, but only by 1 MMT from 157 to 156, while the rest of the market is pegging Brazil soybean production at 153 MMT - Conab adjusted their number down to 149 MMT. USDA left Argentina's soybean production estimate unchanged at 50 MMT.

- Soybean meal: Soybean meal prices were under pressure last week, with renewed selling from Managed Money as reported by the CFTC. The latest US export sales were also disappointing with 200 KT for the week ended February 8, below the trade estimates range around 0.25-0.45.

DL Forecast has been bullish over the last week capturing some of the realized rally. Forecast trajectory is still bullish until mid-February.

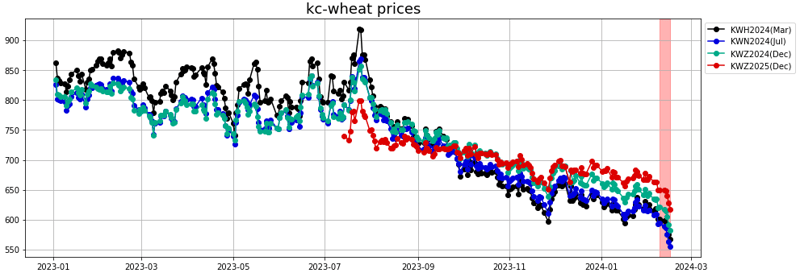

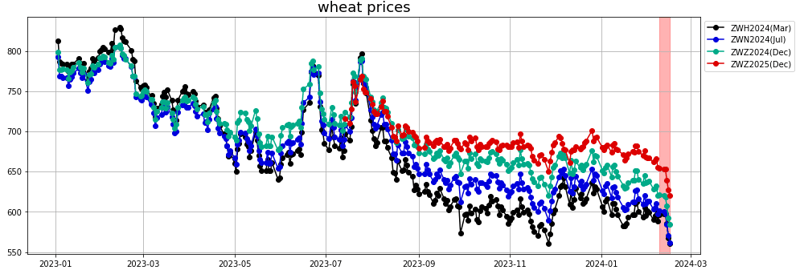

- Wheat: No significant updates in the WASDE release on February 8th. The wheat market stayed relatively stable that week.

The wheat export bookings were 349,286 MT for the week of 2/8 according to the USDA’s FAS data. That was a ~30k MT decrease from the week prior and near the lower end of the expected range, but was up 66% from sales during the same week last year. USDA had shipments at 405k MT for the week, which brought the season total to 11.5 MMT. That still trails last year by 11%, though the +72% of unshipped sales on the books has wheat commitments at 17.6 MMT compared to 16.5 MMT at the same time last year.

Vegoils

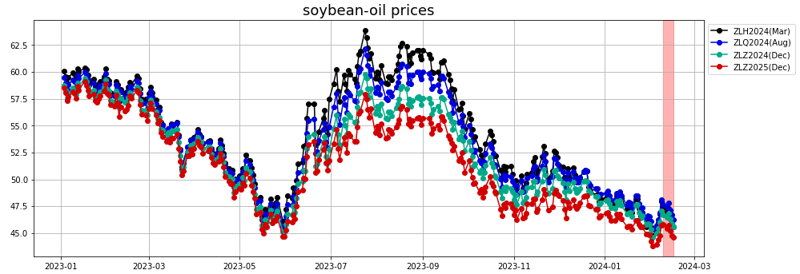

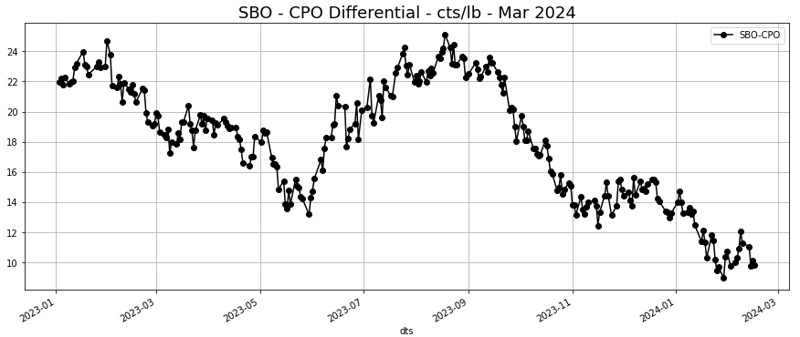

- Soybean oil: NOPA (National Oilseed Processors Association) published their monthly number for January on February 15th. Despite a lower crush number than anticipated (at 185.78 Mbu this remains a record crush number for the month of January), the soybean-oil stocks grew seasonally to reach 1.5 billion pounds, the highest number since July 2023 (but still below the level of the last 5 years)

Forecasts had been bullish for the last week and did not anticipate this move down. Still bullish going forward albeit less aggressively.

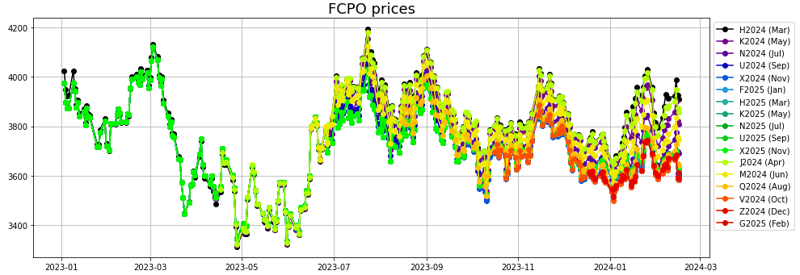

- Palm oil: Earlier in February, palm oil prices rallied strongly because Malaysia's palm oil stocks fell more than expected to their lowest in six months at the end of January as production plunged to the lowest level in nine months amid steady exports, the industry regulator said on Tuesday.

However, last week, Malaysian palm oil futures started to lose steam again because of a sharp drop in exports from the world's second-biggest producer of the tropical oil. Exports of Malaysian palm oil products for February 1-15 fell by 10.8% to 17% from the previous month, two cargo surveyors reported on Thursday.

At the same time, decline in soybean-oil prices pressured palm oil.

The forecast had been slightly bearish as of a week ago but is now bullish following the sell-off.

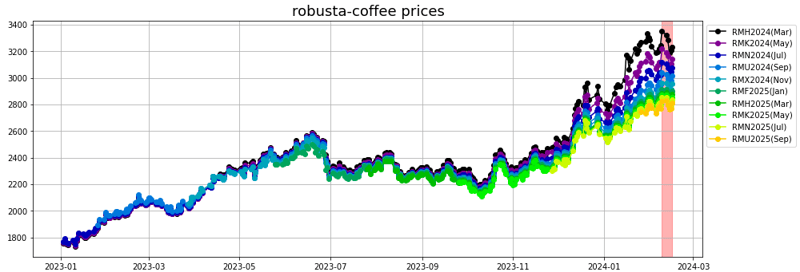

Softs

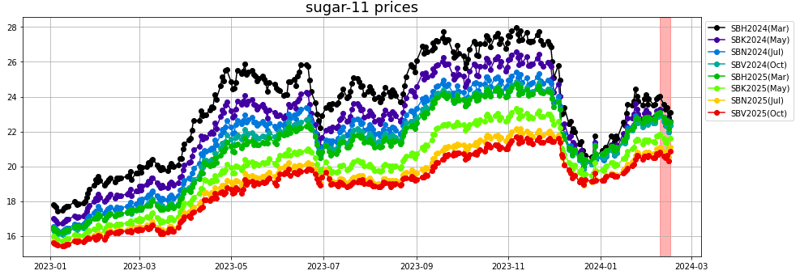

- Sugar: Raw & White sugar: Dealers said output growth in top producer Brazil remains very strong, and that poor crops in India and Thailand are mostly priced in.

What that means is sugar prices have likely found a longer-term ceiling of around 24 cents, unless the dry weather in Brazil worsens or hurts the crop more than expected.

Dealers noted the market is falling even when Brazilian mills, who are usually sellers in futures, are off due to Carnival holidays.

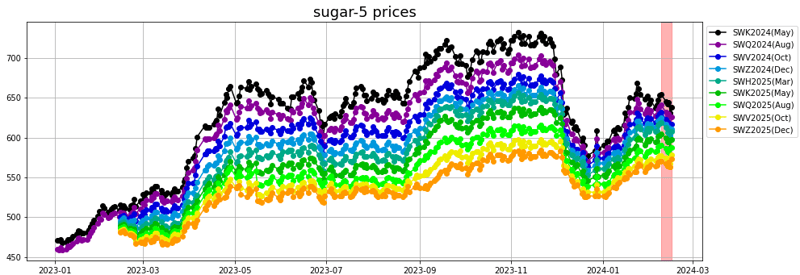

Forecast for sugar #11 has been bearish over the last couple of weeks and is still expecting weakness going forward. Forecast for sugar #5 had been flattish and is still expecting some supported price on the short-term before a gradual rally back above 700 $/MT.

White sugar: There was chat among traders of a better end of crop in India, with some wondering if the government would allow limited exports.

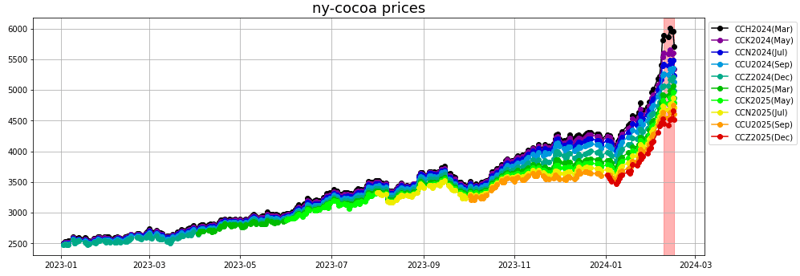

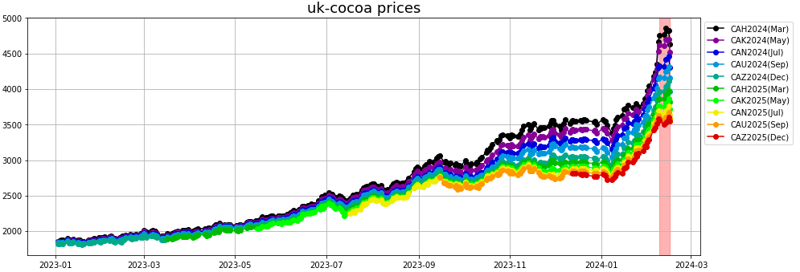

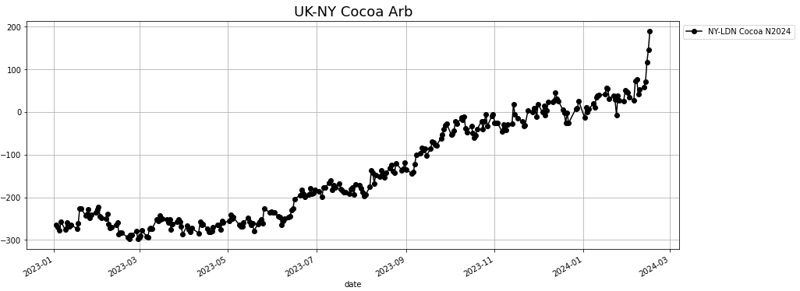

- Cocoa: Cocoa futures fell sharply on Friday as speculators decided to liquidate part of their long position after strong gains this year.

Dealers said speculators decided to sell after the market failed to continue the recent rise to all-time highs.

"It was profit taking, along with some concerns about demand as retail prices rise," said a U.S.-based cocoa broker, adding that the market remains supported in the medium term. "From a S&D point of view, nothing has changed," he said, stressing that price cover by the industry will get smaller towards the next quarters.

Ghana's Cocobod will use part of a $200 million World Bank loan to rehabilitate plantations destroyed by the cocoa swollen shoot virus, the cocoa sector regulator's deputy CEO in charge of operations said.

Ivory Coast's Cocoa and Coffee Council will not default on its export contracts despite a drop in cocoa production since the start of the October-to-March main crop, CCC's managing director Yves Brahima Kone said.

Forecast had been bearish as of last week. Following the latest rally, the forecast trajectory adjusted to be more flattish short-term before weakening during the second half of February.

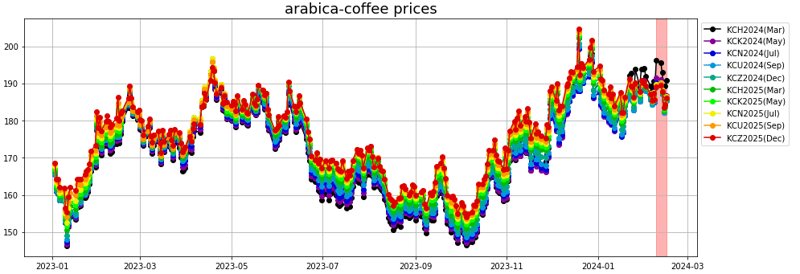

- Coffee: Arabica: Rains in top producer Brazil are boosting the outlook for coffee crops, while rising ICE-certified stocks are also weighing on prices.

ICE arabica stocks rose to 307,262 bags on Friday, and there are 65,717 bags pending grading.

DL model: Forecast has been slightly bearish for the past week and is still expecting some slight weakness in February.

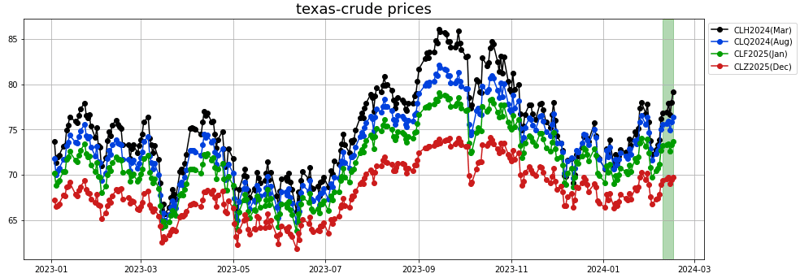

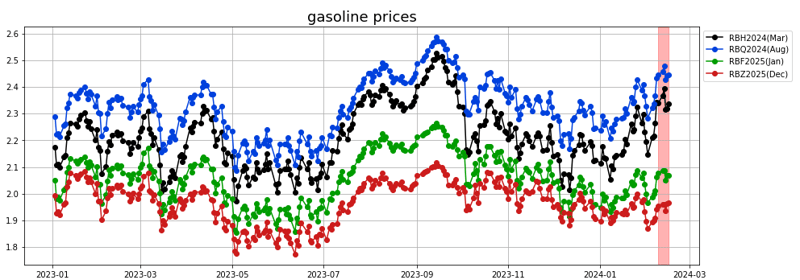

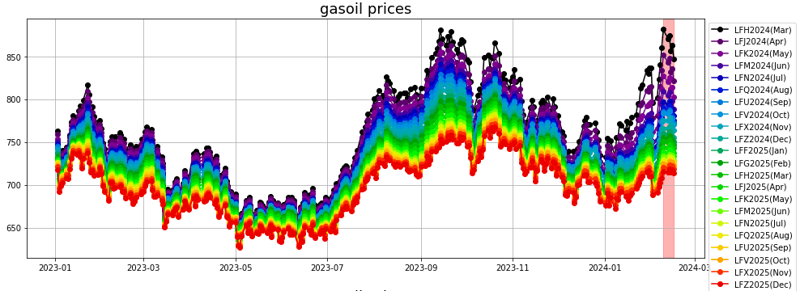

Energy

- Crude oil: Large rebound in the crude complex over the last two weeks boosted by a geopolitical premium as the ceased fire failed to materialize. EIA statistics were supportive two weeks ago but weaker for crude last week. An increasing backwardation in the front of the WTI and Brent forward curve hinted at some effective physical tightness, all the more surprising as we are in the refinery maintenance season.

- Gasoline: It seems that the gasoline situation turned a corner, with two successive weeks of inventory draws, potentially hinting at an early onset of the seasonal draw period for gasoline. Outages and maintenance at large refineries in the US supported the product cracks.

- Diesel/Gasoil: Diesel has remained very volatile, with a very strong week in early February, seeing the price of gasoil reaching back to the highs seen last September, while last week saw this strength erased partially.

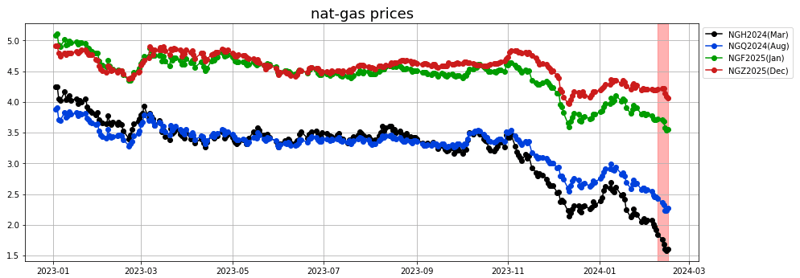

- Natural gas: The continuing warmer-than-normal winter in the US, combined with a rebound in production led the price to new lows. While this price level should be enough to incentivize additional power burn, it seems that the market may need to go low enough to trigger a producer response to avoid filling up storage by October 2024.

Receive Market Report Notifications

Receive Market Report Notifications

Sign up below to get alerts directly in your inbox when a new Market Report is released.